How institutional capital actually moves.

Notes on capital-readiness, fundraising strategy, and what investors actually fund — written by the team that takes founders to market every week. No platitudes. No vague advice. The patterns we see, said plainly.

Published monthly · Market data, narrative craft, founder mistakes

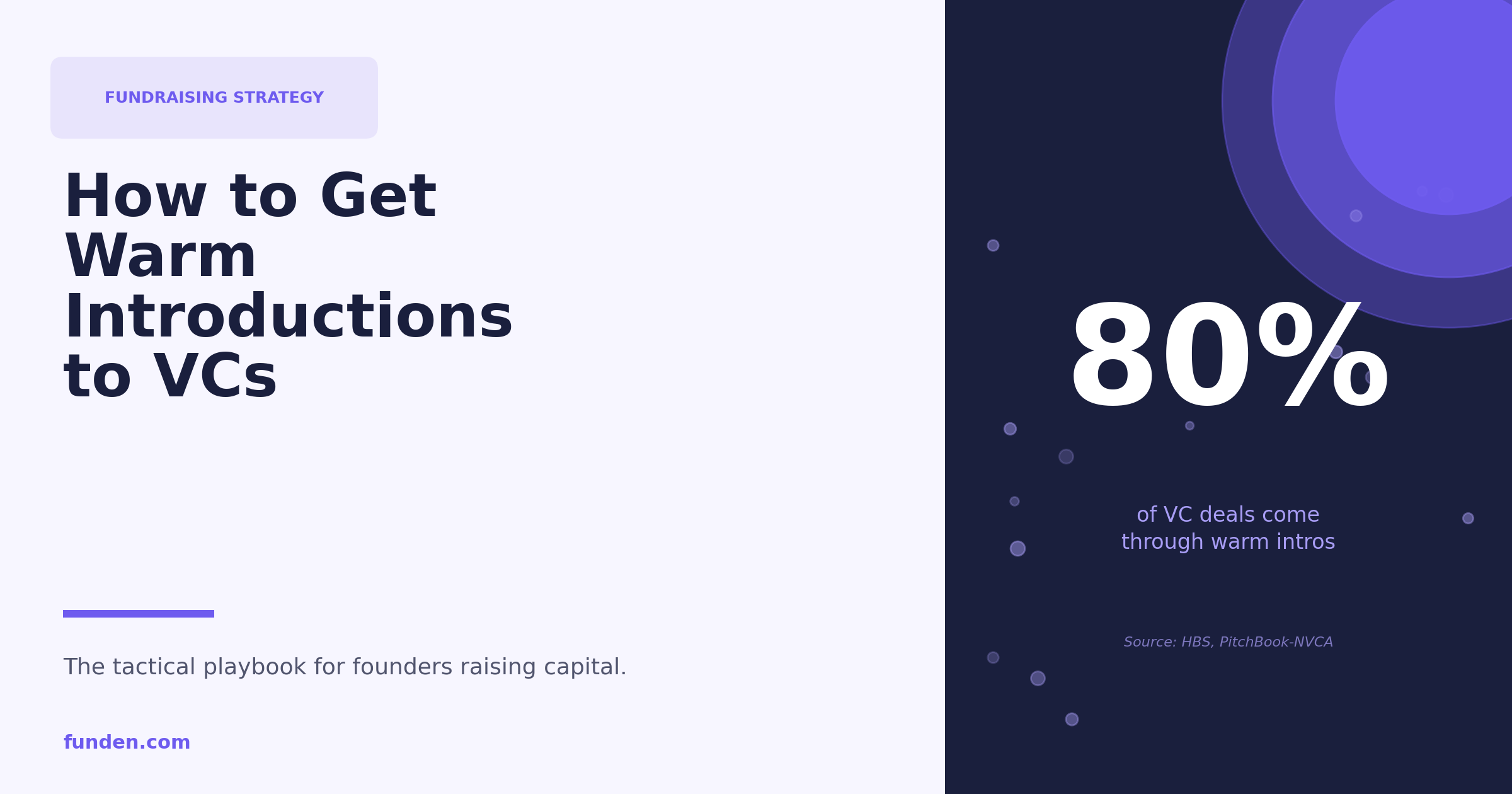

How to Get Warm Introductions to VCs: A Tactical Guide

A Harvard Business School survey of nearly 900 institutional VCs found that roughly 58% of funded deals originate through professional networks, investor referrals, or portfolio company introductions.

Latest notes

Recent thinking on market structure, founder behaviour, and what investors really underwrite.

The 10 Best Fundraising Platforms for Startups in the USA (2026)

Funden is a capital advisory firm built around a single observation. Most founders fail their raise because the deal isn't ready, not because the intros are missing.

The 10 Best Fundraising Platforms for Startups in the USA (2026)

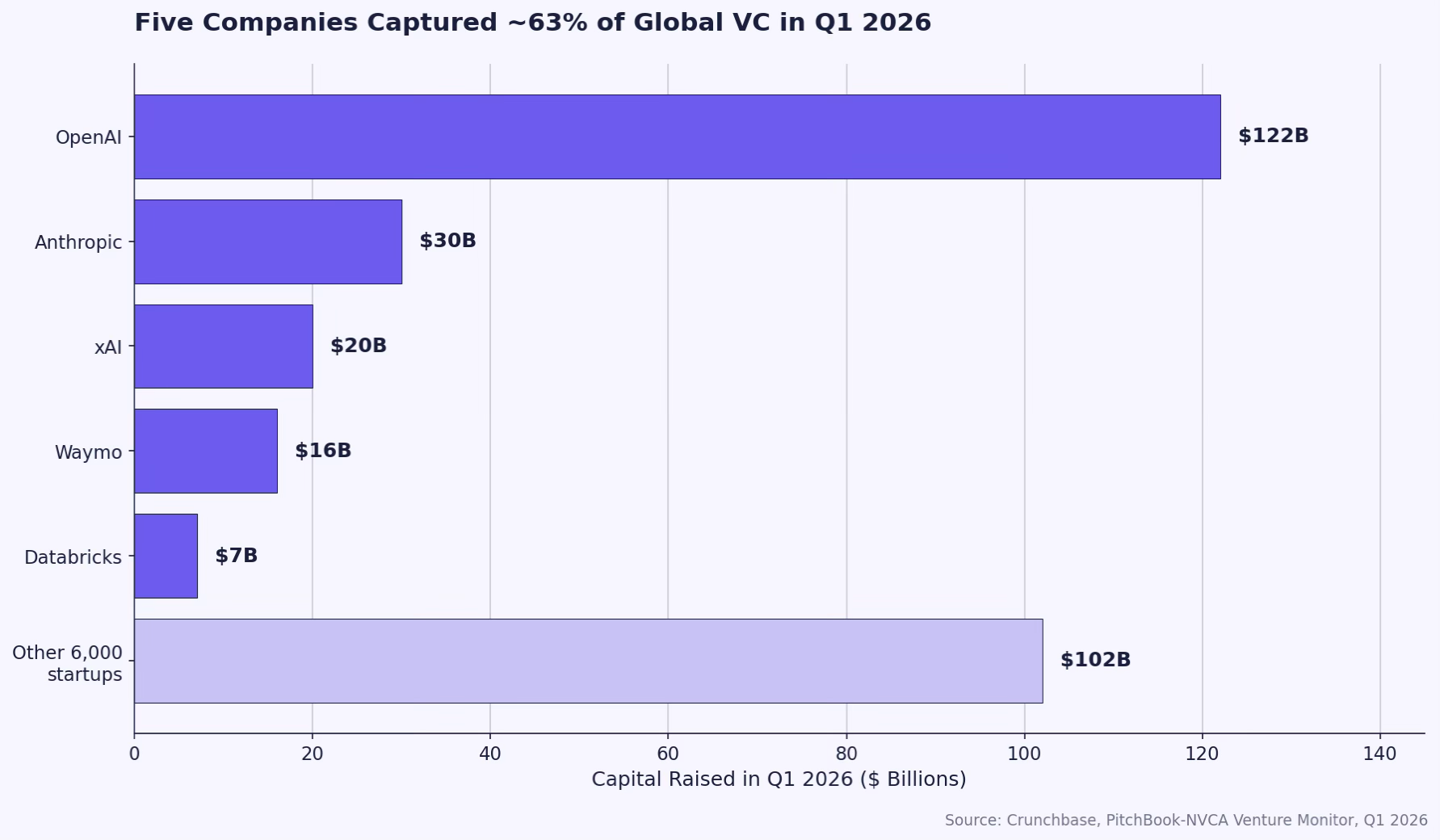

Q1 2026 set every funding record on the books. $297 billion was deployed globally, a 150% jump year over year. Four AI deals captured $188 billion of that, roughly 63% of the quarter. Strip those out and the remaining 6,000 startups split about $109 billion.

That gap is the story of fundraising in 2026. Capital exists. Access to it does not.

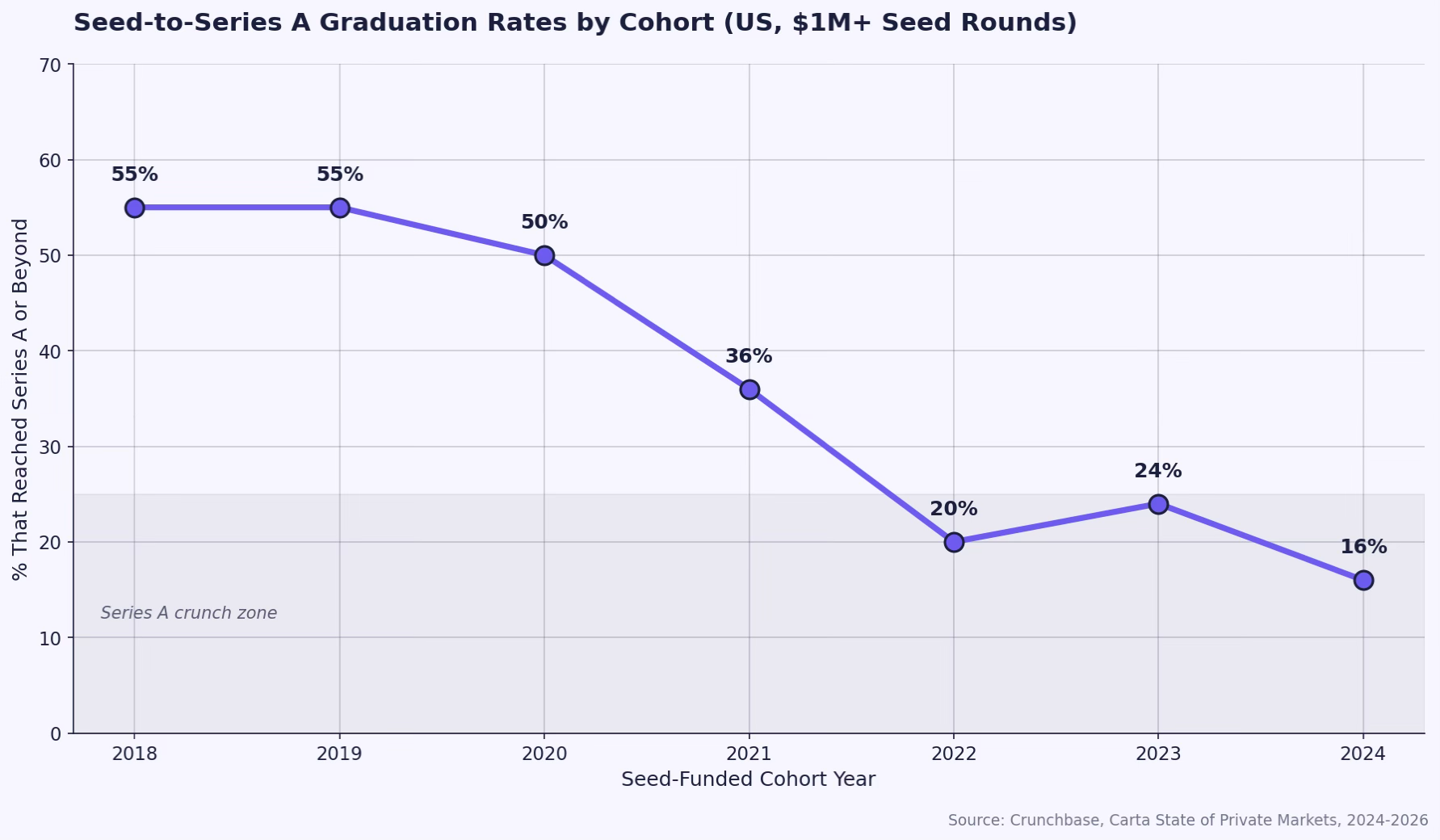

Crunchbase data shows just 16% of 2024-cohort startups that raised a $1M+ seed have graduated to Series A. Compare that to 55% or more for pre-2020 cohorts. The path from one round to the next has compressed in dollars and stretched in time. According to Carta data on 3,365 US startups, 39% of companies now take three or more years between seed and Series A, double the rate from 2019.

That's why fundraising platforms matter more than ever. They're the rails founders use to reach capital that no longer flows freely. Not every platform serves the same need. Some run institutional rounds. Some crowdsource from retail. Some specialize in syndicates, secondaries, or warm introductions. Picking the wrong one wastes 90 days you can't get back.

Below, the ten fundraising platforms US founders should evaluate in 2026, ranked by depth of service, founder fit, and track record.

How fundraising platforms divide in 2026

Fundraising platforms in the US split into five rough categories:

- Capital advisory and investor matching (high-touch, institutional)

- Equity crowdfunding (Regulation CF, Regulation A+, Regulation D)

- Angel syndicates and rolling funds

- Secondary marketplaces (pre-IPO liquidity)

- Hybrid and vertical-specific platforms

Founders typically use one or two categories per round. Series A founders pulling from institutional VCs lean on advisory and syndicates. Pre-seed founders without strong investor networks may run a Reg CF campaign alongside angel outreach. A late-seed company might use a secondary marketplace to give early employees liquidity while the formal round closes.

1. Funden: Best for institutional capital advisory (Pre-Seed to Series B)

Funden is a capital advisory firm built around a single observation. Most founders fail their raise because the deal isn't ready, not because the intros are missing.

The firm runs an Assisted Fundraising program for founders raising $1M to $15M+ across Pre-Seed through Series B. Engagement starts with a 30-minute call to pressure-test the narrative, structure, and readiness of the deal. If accepted, founders go through deal benchmarking, narrative stress-testing with real investors, and institutionalization of the deal before warm introductions to a network of 800+ partner VCs, family offices, and angel networks.

Track record (as of 2026):

- 1,300+ founders supported through the capital readiness process

- $180M+ in capital raised by Funden-supported companies

- 500+ institutional investors engaged per deal

- 2,000+ warm introductions made

- Backed by FE International, the firm behind $50B+ in M&A transactions across 2,000+ deals globally

Stages served:

Pre-Seed, Seed, Series A, Series B

Offices: San Francisco, New York, London

Cost model: Monthly retainer. No success fees, no equity taken from the round.

Best fit: Founders who want a real diagnosis before going to market. Companies that have the fundamentals but need help institutionalizing the deal, refining the narrative, and getting in front of investors aligned to their stage and thesis.

The differentiator: most platforms are self-serve. Funden runs a process. Founders work with the team to surface what's actually broken in the deal before investors see it, which is the difference between closing in 90 days and burning six months on rejections.

Apply at funden.com or book a call with the Funden team.

2. AngelList: Best for syndicates and rolling funds

AngelList pioneered online syndicates in 2013 and remains the default platform for tech founders raising from angels and emerging VC fund managers.

The platform supports $171B+ in assets, 72,000+ active investors, and $10.7B+ raised by active startups, including more than 100 unicorns. Rolling Funds, launched in 2020, let GPs deploy capital from LPs who commit quarterly, expanding the platform to more than 10,000 active fund managers.

- Best for: Founders raising $250K to $5M who have warm intros to syndicate leads or are already in a hot deal that will fill quickly.

- Fees: Roughly 20% carry on syndicate profits, varies by fund manager.

- Trade-off: Syndicates work best when there's a clear lead investor setting terms. Used as a primary fundraising channel without an anchor, syndicates often stall.

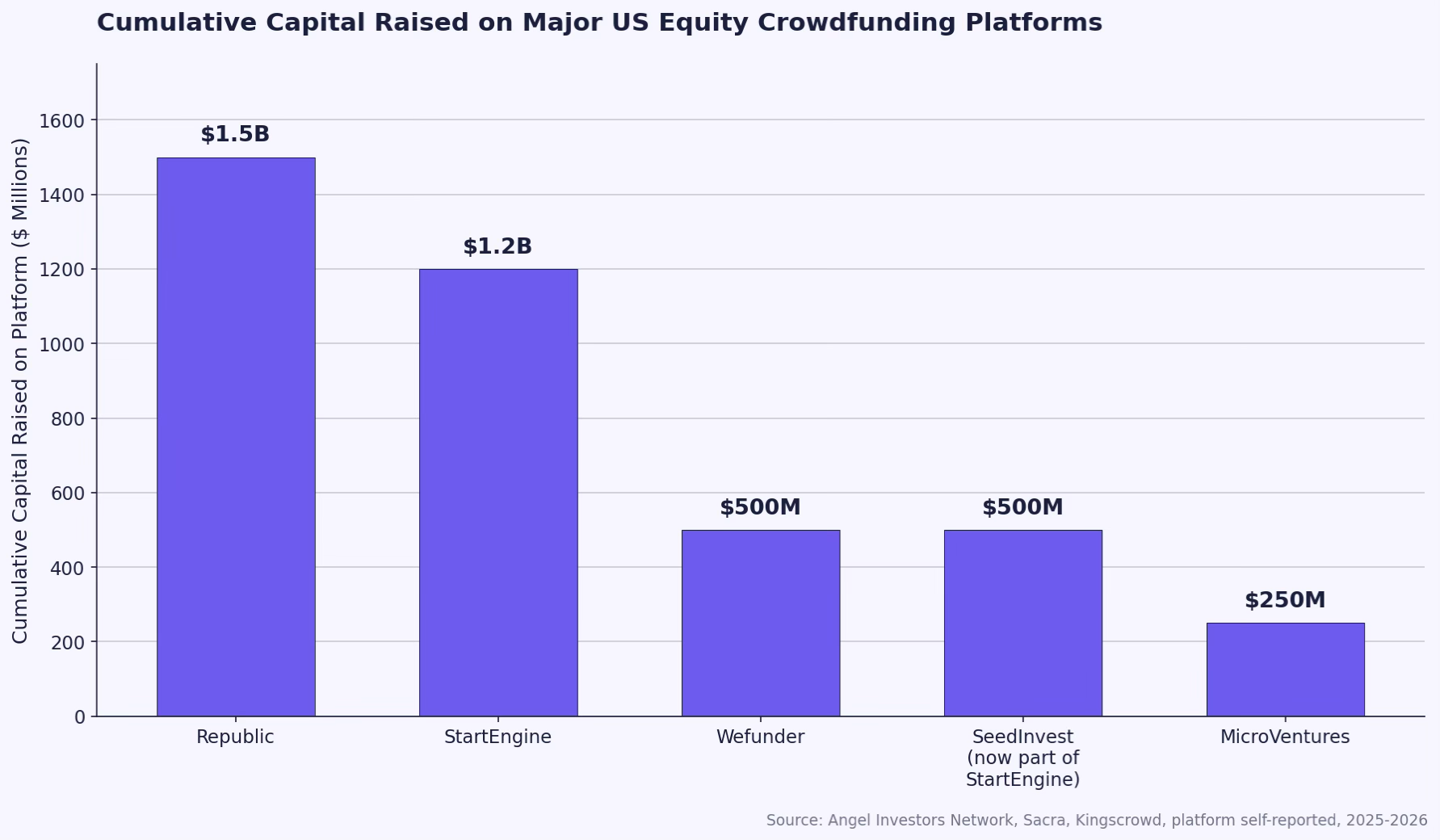

3. Wefunder: Equity crowdfunding leader by volume

Wefunder dominates Regulation CF deal volume in the US, holding roughly 33% of total Reg CF dollars raised. Over its life, the platform has facilitated more than $500M across 2M+ registered investors.

- Best for: Consumer brands, breweries, restaurants, mission-driven companies, and B2B startups with existing customer communities.

- Fees: 7.5% platform fee on the first $500K raised, 5% thereafter. 2% equity in most deals.

- What it does well: Community-driven model where investors vote on featured campaigns. Strong fit for companies that can mobilize an existing email list.

The Reg CF cap raised from $1.07M to $5M in 2021, which materially changed what's possible on the platform. A well-run Wefunder campaign can now close a full seed round.

4. Republic: Equity crowdfunding plus secondary market

Republic has facilitated $1.5B+ raised across startups, real estate, and crypto since launch. The platform serves 3M+ registered investors and has expanded into Mirror Tokens (digital instruments tracking private company values) and a venture fund that co-invests in top-performing platform campaigns.

- Best for: Tech and consumer startups looking for accredited investor exposure alongside retail capital. Roughly 50% to 60% of Republic's investor base is accredited, the highest mix among major Reg CF platforms.

- Fees: 6% cash plus 2% equity on capital raised.

- Strategic angle: If a Republic raise performs well, the firm's institutional arm may lead the follow-on Series A. That feedback loop doesn't exist on other crowdfunding platforms.

Republic Capital reported two IPOs from its portfolio in 2025 with three more queued for 2026.

5. StartEngine: Largest Reg A+ volume

StartEngine has raised $1.2B+ across 1,000+ campaigns since 2014, with 1.8M+ registered investors. Kevin O'Leary's involvement as Chief Strategy Advisor brings media access (Shark Tank features, CNBC interviews) that other platforms can't match.

- Best for: Hardware, deep tech, and consumer hardware startups. Higher-volume campaigns ($1M to $5M Reg CF or $5M to $75M Reg A+).

- Fees: 6% to 8% of capital raised. 2% equity component negotiable.

- Success rate: Reg CF campaigns on StartEngine close at 90.8%, the highest in the category.

6. MicroVentures: Curated equity crowdfunding for accredited investors

MicroVentures runs a tighter selection process than the major Reg CF platforms. Less than 5% of applicants get listed, which compresses founder timelines but improves campaign quality on the platform.

- Best for: Series A-ready companies with strong fundamentals that want an accredited-investor-only marketplace. Companies in internet software, media, green tech, mobile, and gaming.

- Track record: Early backer of Airbnb and Slack, among others.

- Fees: All-or-nothing structure. If the campaign misses the target, the company keeps nothing.

7. DealMaker: Best for white-label fundraising infrastructure

DealMaker isn't a marketplace. It's the back-end infrastructure that processes investments for issuers who run their own raise pages. Wefunder now considers DealMaker its primary competitor in Reg CF, replacing Republic in that position.

- Best for: Companies that have an audience and want to capture investors directly through their own website, not a third-party marketplace.

- Fees: Software plus processing fees. No platform take of equity.

- Use case: Brands with significant direct-to-consumer reach or B2B companies running structured Reg D 506(c) raises.

8. Fundable: Hybrid rewards and equity for early-stage products

Fundable, owned by Startups.com, offers a hybrid model combining equity crowdfunding with rewards-based campaigns. The platform is built for software, hardware, and consumer product companies that want to layer product pre-orders on top of equity capital.

- Best for: Pre-seed and seed-stage product companies that can monetize through customer pre-sales while also raising equity.

- Fees: Subscription-based. Money and shares change hands outside the platform.

- Trade-off: Fundable is more of a profile-and-pitch service than a closed marketplace. Founders contact investment targets directly.

9. Hiive: Secondary marketplace for private stock

Hiive isn't a primary fundraising platform. It's a marketplace for buying and selling shares in VC-backed companies before IPO. For founders, the value is offering early employees and angels a liquidity path before the formal exit.

- Best for: Late-seed to Series B companies whose early employees and angels want partial liquidity. Companies looking to bring in new investors via secondary sales.

- Investor base: Accredited investors and family offices buying private shares directly.

- Why it matters in 2026: With time-to-IPO stretching for most VC-backed companies, secondary liquidity has become a retention tool. Hiive, Forge Global, and EquityZen are the three platforms most US founders will interact with for this purpose.

10. OurCrowd: Global accredited investor platform

OurCrowd is an Israeli-founded platform with US operations, serving accredited investors only. The platform has facilitated billions in funding across a global portfolio of 400+ companies since 2013.

- Best for: Startups looking for international accredited capital, particularly in deep tech, defense, healthcare, and AI.

- Fees: Mix of management fees and carry, structured like a fund.

- Difference: OurCrowd uses an SPV model. Each deal forms its own investment vehicle, so founders deal with one entity on their cap table, not hundreds of individual checks.

How to pick the right platform for your stage

Match the platform to the stage and the audience you have.

Pre-Seed ($250K to $1M):

AngelList syndicates or a Reg CF raise on Wefunder if you have an audience. Skip institutional advisory until you've validated product-market fit.

Seed ($1M to $5M):

Funden if you want institutional VCs. AngelList for syndicate-led rounds. Wefunder or StartEngine if you have a consumer brand or product audience.

Series A ($5M to $15M):

Funden for institutional fundraising. Republic or MicroVentures only if you want a strategic retail layer alongside the institutional round.

Series B+ ($15M to $50M):

Funden for advisory and warm intros to institutional capital. Hiive for secondary liquidity for early employees. Skip Reg CF entirely at this stage.

The platform you choose tells investors something about how you think about the raise. Reg CF works for some companies and signals weakness for others. Institutional advisory works when you have the fundamentals to back it up. The choice matters more than founders typically assume.

The deal makes the platform work, not the other way around

The fundraising platform you choose matters less than whether your deal is actually ready for the platform you choose. Most founders spend six to twelve months on outreach before realizing what was broken in the deal. By then, the calendar, the cap table, and the runway have all worked against them.

Funden exists to compress that timeline. The team has supported 1,300+ founders, engages 500+ institutional investors per deal, and has helped portfolio companies raise $180M+ to date. Backed by FE International, the firm runs a structured process: deal benchmarking, narrative stress-testing with real investors, institutionalization, and warm introductions to a network of 800+ partner VCs.

If you're raising between $1M and $15M+ and want a real diagnosis before going to market, book a 30-minute call with the Funden team. The best outcome of that call is clarity, whether or not we end up working together.

Fundraising Ideas in 2026: What Actually Works Now

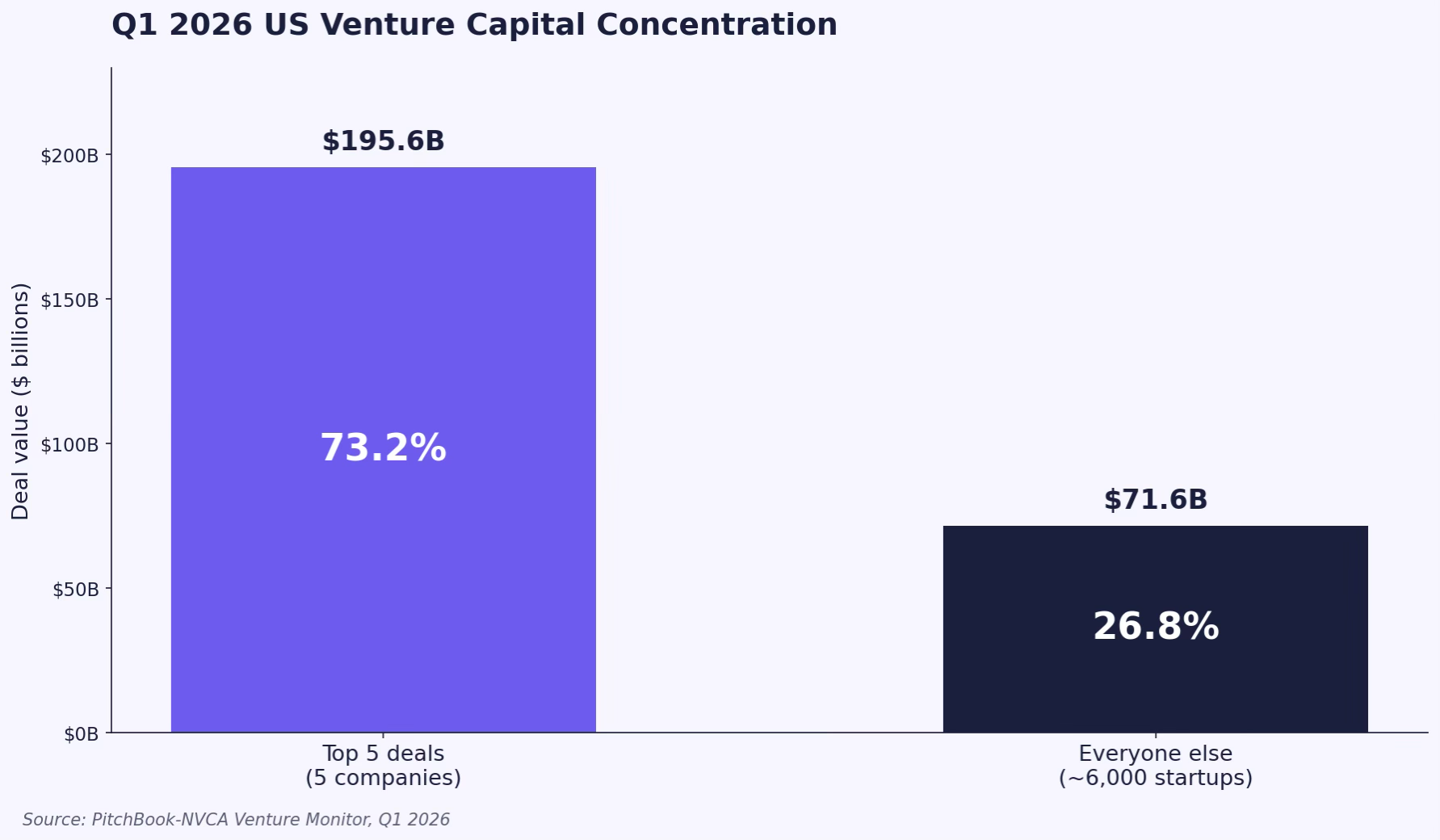

In Q1 2026, US startups raised $267.2 billion. Five companies took roughly three-quarters of it. According to the PitchBook-NVCA Venture Monitor, remove the top five deals and quarterly venture funding falls 73.2%. The headline numbers look like 2021 came back.

Fundraising Ideas in 2026: What Actually Works Now

In Q1 2026, US startups raised $267.2 billion. Five companies took roughly three-quarters of it. According to the PitchBook-NVCA Venture Monitor, remove the top five deals and quarterly venture funding falls 73.2%. The headline numbers look like 2021 came back. Underneath, the experience for most founders is closer to 2023.

If you are not OpenAI, Anthropic, xAI, Waymo, or one of the handful of frontier labs absorbing sovereign-scale checks, your raise in 2026 is going to look more like a long, structured search than a competitive auction. Median time between a seed and Series A reached 616 days, more than 20 months, according to Carta. SVB summarised the dynamic plainly in its H1 2026 State of the Markets: the venture market is bifurcated, with abundance at the apex and measured scarcity elsewhere.

What follows is not a generic list of fundraising tips. These are seven strategies we see closing rounds right now, drawn from current investor behaviour and from the patterns we observe working with founders preparing to go to market. If you are in the 99% of founders not raising on the strength of being a frontier model, this is the playbook that fits the actual market you are raising into.

1. Build a deal investors can underwrite, not a story you can pitch

The most common mistake in 2026 is treating fundraising like a marketing exercise. Founders polish the deck, rehearse the story, build a target list, and start emailing. Three months later they have a pile of soft passes and no idea why.

The reason is structural. With $255.5 billion of AI capital deployed in a single quarter and most of it concentrated in fewer than ten companies, partners at non-AI-focused funds are under pressure to make every check count. A clean narrative is no longer enough. Investors are underwriting deals the way an acquirer would: looking at unit economics, retention, defensibility, team composition, capital efficiency, and exit pathways before they decide a meeting is worth taking.

Treat your raise like an institutional transaction from day one. Before you build the deck, write the investor memo. Stress-test the financials. Identify the three objections any sharp partner will raise and prepare for them with data, not adjectives. The founders we see closing rounds in 2026 spend longer preparing and less time pitching. That ratio is almost always inverted in struggling raises.

A useful caveat: this advice applies to priced rounds and any SAFE above roughly $1.5M. For a $500K friends-and-family note from people who already believe in you, the deal-readiness work matters less. For everything else, it is the work.

2. Run the round like a search for one lead, not a poll of 100 maybes

Spray-and-pray outreach to 200 funds is a comfort behaviour. It feels productive. It rarely closes a round. The mechanics of a priced round still require a lead investor willing to set terms, write the largest check, and pull the rest of the syndicate along. Until you have a lead, you do not have momentum, no matter how many partner meetings you take.

DocSend's pitch deck research has consistently found that decks resulting in a meeting average about three and a half minutes of investor reading time, and that the correlation between number of investors contacted and dollars raised is weak. Reaching the right ten investors matters more than spraying 200.

Build a short list of 30 to 50 funds whose thesis, stage, and check size actually match your round. Within that list, identify five to ten potential leads. Sequence your outreach so the most likely leads are not the first conversations. Open with two or three investors whose feedback you respect but who are unlikely to lead, use those meetings to pressure-test the pitch, then move into the lead conversations once the narrative is sharp.

Run parallel processes. A lead investor will move faster if they sense competitive tension, even if that tension comes from one credible alternative rather than five. Sequencing is not deceptive, it is professional.

3. Engineer warm intro paths 90 days before you open the round

Cold outreach response rates to investors sit around 3 to 5%. Warm intros from a trusted source pull that into the 15 to 20% range. The math is straightforward, and yet most founders treat the warm-intro problem as something to solve once fundraising has started. By then, it is already too late.

Map your target investor list to your existing network roughly 90 days before you plan to open the round. For each fund on the list, identify two to three credible introduction paths: a portfolio founder, a co-investor at a previous round, an angel they trust, an operator they have backed. Most founders find they already have one or two paths into 60% of their list. The remaining 40% requires deliberate relationship building, which is the work that needs the 90-day runway.

The intro path matters as much as the existence of an intro. A passing forward from someone who barely knows you signals nothing. An intro from a portfolio founder who can speak to specifics about your team or product is a different document entirely. The strongest signal is what the warm-intro literature calls a hot intro: the connector is putting their own check in. That is the version that closes seed rounds.

If you do not have those paths yet, the 90 days before you raise are when you build them. Show up in the conversations the people you want intros from are actually in. Help before you ask.

4. Stack non-dilutive capital before you sell equity

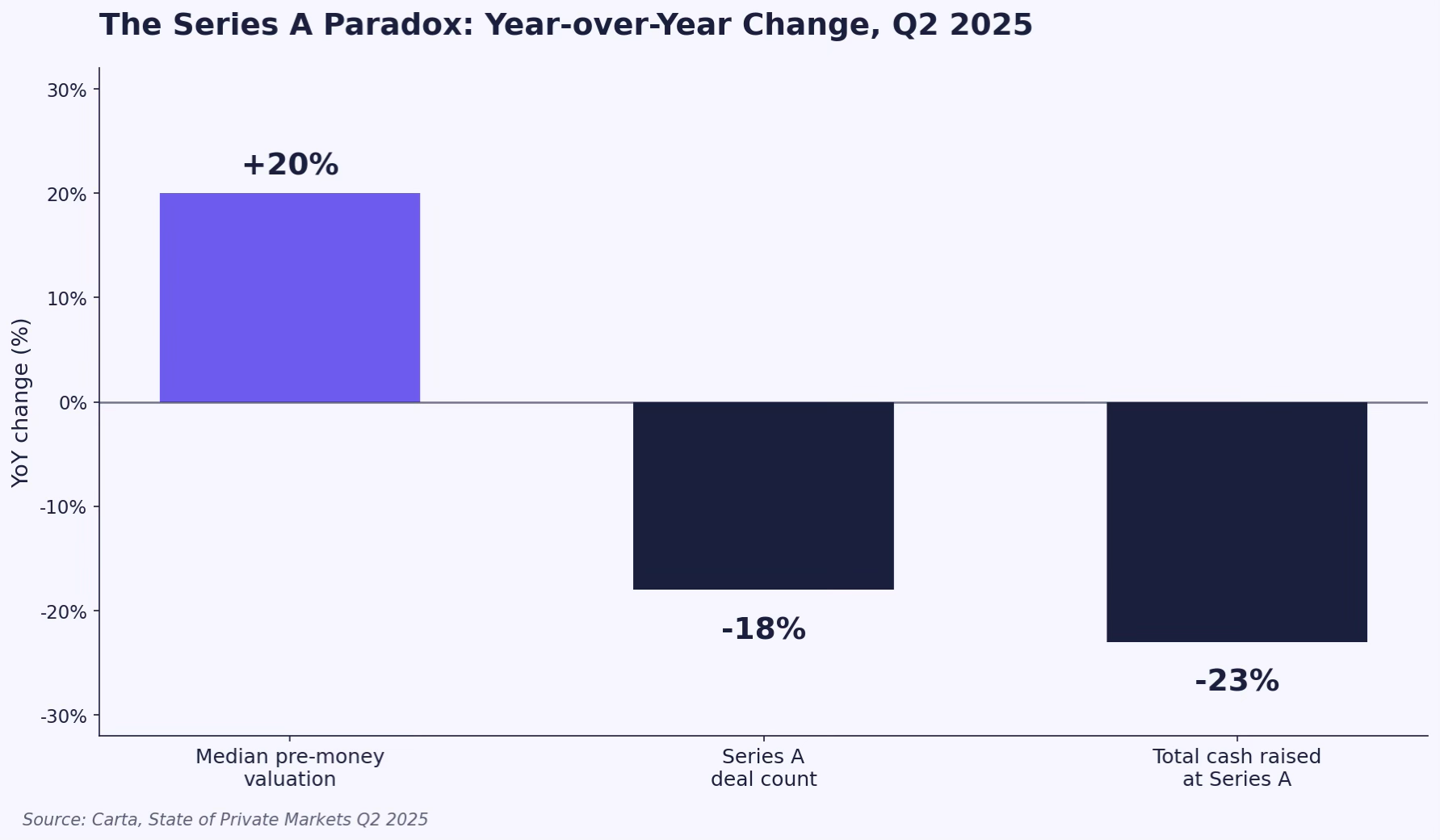

Carta's most recent State of Private Markets report showed an unusual pattern: median pre-money valuations at Series A climbed to a record $49.3 million in Q3 2025, while Series A deal count and total cash raised both fell substantially year-over-year. Valuations are up. Round counts are down. That gap is what makes non-dilutive capital so useful in 2026.

Every dollar you raise through revenue-based financing, venture debt, a customer prepayment, or a strategic grant is a dollar you do not sell equity for at a price the market may not actually support. Venture debt in particular has matured into a real option for VC-backed companies looking to extend runway between rounds without taking a flat or down round on equity.

The pattern that works: close a smaller equity round than you initially planned, then layer venture debt or revenue-based financing on top to extend runway by another six to nine months. This buys you the time to hit the milestones that move you into a stronger position for your next priced round. The instrument matters. Venture debt usually requires recent VC backing and has covenants worth reading carefully. Revenue-based financing requires predictable recurring revenue. Customer prepayments require a real product and a customer with reason to lock in early pricing.

Caveat for early-stage founders: non-dilutive capital is a runway extension tool, not a substitute for the equity round itself. If your unit economics are not yet proven, debt of any kind compounds the risk. This strategy works best after seed and into Series A or B.

5. Use CVCs as a strategic second check, not your lead

Corporate venture capital has become one of the most consistent sources of capital in the post-2022 market. According to Harvard Law School Forum's 2026 venture outlook, strong AI-adjacent companies are attracting CVC interest at every stage, and corporates have stepped into gaps left by traditional VCs in less hot categories.

The strategic logic is straightforward. A CVC investor often brings distribution, technical infrastructure, enterprise pilots, and credibility with the kinds of customers you are trying to win. For a fintech selling into banks, a strategic investment from a regional bank's venture arm can shorten an 18-month sales cycle dramatically. For a vertical SaaS company, a CVC partner inside the industry you sell into is a market signal that compounds.

The structural caveats are real, though. CVCs often move slower than financial VCs, can have shifting priorities tied to internal leadership changes, and carry signalling risk if other VCs interpret their presence as a sign you are pre-positioning for acquisition. The pattern that works in 2026: lead with a financial investor, then add a CVC as a follow-on for strategic value. Letting a CVC lead at seed or Series A is the move most experienced investors quietly advise against.

Where this breaks down: for deep-tech or hard-tech companies where the only viable customer is the corporate, leading with strategic capital sometimes makes sense. Evaluate based on who actually buys your product, not on generic playbooks.

6. Pick the instrument that matches the math

SAFEs have become the default at the earliest stages for good reason. Carta data shows SAFEs now account for around 90% of pre-seed deals and roughly 64% of seed rounds. They close faster, cost less in legal fees, and defer the valuation negotiation to your Series A.

What founders underestimate is how stacked SAFEs compound dilution. Each post-money SAFE only dilutes existing shareholders, which means each new SAFE round dilutes the founders and the prior SAFE holders, not itself. By the time you reach a priced Series A, four or five layered SAFEs at rising caps can leave founders meaningfully more diluted than a single priced round at the same effective valuation would have produced.

The framework that works in 2026 is roughly: under $1.5M raised mostly from angels, use a SAFE. Above $3M with an institutional lead, priced rounds usually serve everyone better, give clearer terms, and avoid the cap-table arithmetic that surprises founders at Series A diligence. Between those two bands, the right answer depends on whether you have a lead willing to set terms and how many existing SAFEs are already on your cap table.

Model both scenarios before you commit. A startup lawyer can build the dilution comparison in an hour. The founders who skip this step are the ones who arrive at their Series A pricing conversation having forgotten that three of their earlier SAFEs convert at caps that materially reduce their post-money ownership.

7. If you have already raised, consider a secondary instead of a bigger primary

One of the structurally new patterns in 2026 is the rise of employee-focused tender offers as a liquidity tool. Carta tracked 396 tender offers in 2025, up 62% from the year prior. Unlike the 2021 era, when secondaries were largely founder-only payouts at buzzy companies, the current wave is structured to reward employees and to give companies a way to retain key staff.

TechCrunch reported on the recent wave: Clay ran an employee tender at a $5 billion valuation, Linear at $1.25 billion, and ElevenLabs authorized a $100 million secondary sale at a $6.6 billion valuation. None of those were ZIRP-era founder cashouts. They were structured liquidity events designed to keep top talent from defecting to OpenAI, Anthropic, or whichever frontier lab is hiring most aggressively this quarter.

For growth-stage companies, a tender offer can replace the function of an oversized primary round. You provide liquidity to employees and early investors without diluting the cap table further, and without forcing a valuation reset that a flat primary round would require. The mechanics are not trivial. You need a willing buyer, board approval, a fair-market-value determination, and clear eligibility rules. But for the right company at the right stage, a secondary is often a more honest tool than a primary you do not strictly need.

Important: secondaries are not a substitute for a real fundraise if you are running out of cash. They work as a retention and liquidity tool when the underlying business is genuinely growing. Trying to manufacture a tender to mask weak fundamentals tends to make the next priced round harder, not easier.

Final Thought

The defining feature of fundraising in 2026 is that the headline numbers and the founder experience have separated. Total capital deployed looks healthy. Most founders raising right now will tell you otherwise. The seven strategies above are not magic, they are the working patterns we see across founders who close rounds in the current market rather than waste a year discovering what the market actually wanted.

The common thread across all of them is that fundraising is no longer about being interesting. It is about being undeniable on the dimensions that matter to investors who have, in 2026, become very selective about where they place their attention.

Funden helps founders institutionalize their deal before going to market. If you are preparing for a raise and want structured feedback on whether the deal is ready, apply at funden.com.

How to Get Warm Introductions to VCs: A Tactical Guide

A Harvard Business School survey of nearly 900 institutional VCs found that roughly 58% of funded deals originate through professional networks, investor referrals, or portfolio company introductions.

How to Get Warm Introductions to VCs:

A Tactical Guide for Founders

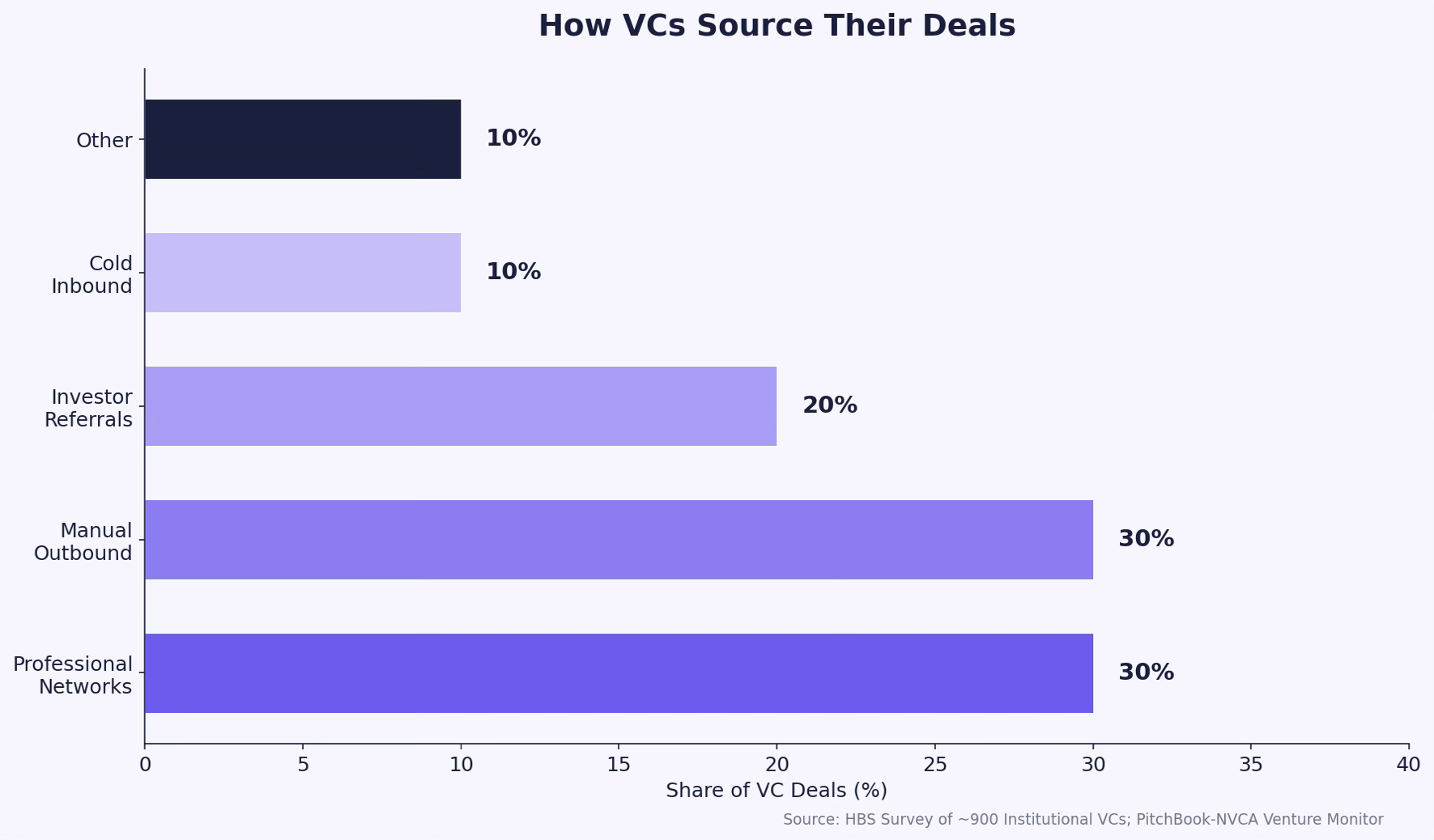

A Harvard Business School survey of nearly 900 institutional VCs found that roughly 58% of funded deals originate through professional networks, investor referrals, or portfolio company introductions. Add manual outbound sourced through relationships and the figure climbs to around 80%. Cold inbound, the channel most first-time founders default to, accounts for approximately 10%.

Those numbers are not new, but the gap is widening. As capital concentrates into fewer deals and fewer firms, per the PitchBook-NVCA Venture Monitor Q1 2026 data, investors have less time and more reasons to filter by trust signals before evaluating business quality. The warm introduction is the highest-signal filter available to them.

This guide is not about networking platitudes. It is a tactical breakdown of how founders can systematically build, request, and convert warm introductions into investor meetings, based on what we see working across hundreds of fundraising processes.

Why Warm Introductions Work (And Why Cold Email Doesn't)

VCs receive 300 to 500 inbound email pitches per month. They read maybe 50 fully. They schedule meetings for 3 to 5. If you arrive as an unvetted email, you are competing with 99 others that day. If you arrive as an introduction from a portfolio founder the investor already trusts, you are competing with the last two meetings before the investment committee.

The difference is not marginal. Warm introduction response rates consistently run 20 to 40%, compared to 1 to 3% for cold outreach. Meeting show rates from warm intros are 85 to 95%, versus 50 to 60% for cold-sourced meetings. The compounding effect through the rest of the funnel is significant: shorter discovery calls, faster diligence, and higher close rates.

This matters because the warmth does not make your company better. It makes the investor's decision-making easier. VCs are pattern-matching machines, and a referral from a trusted source is a shortcut through the noise.

Not All Warm Introductions Are Equal

Founders often treat all introductions as interchangeable. They are not. The conversion gap between different types of connectors is massive.

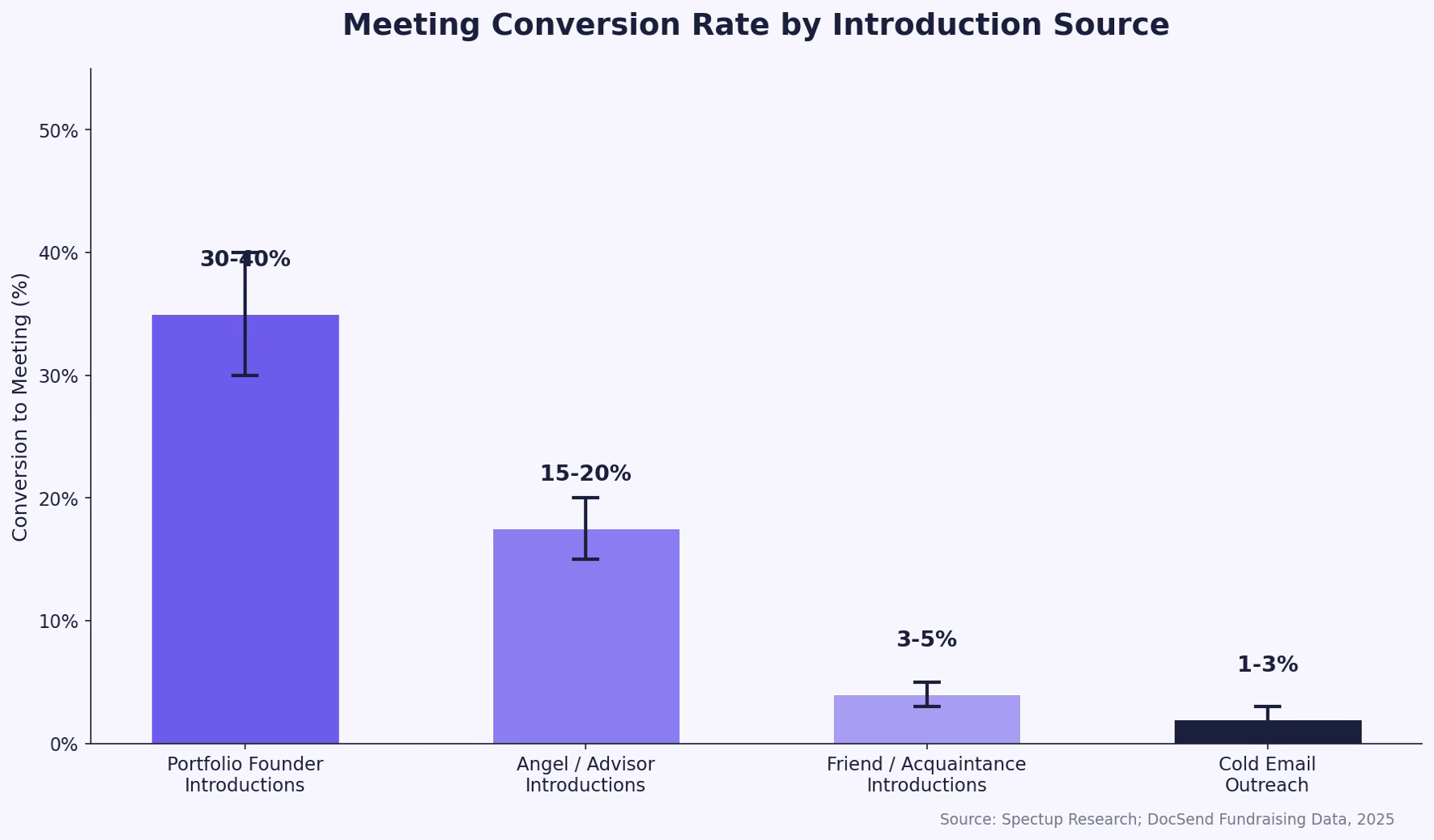

Portfolio founder introductions, where someone who has already been funded by the target VC makes the connection, convert to meetings at 30 to 40%. These carry the most weight because the connector has a direct, ongoing financial relationship with the investor. Their reputation is on the line.

Angel investors and advisors convert at 15 to 20%. They have credibility in the ecosystem, but their relationship with the specific VC may be more distant. Friends and acquaintances sit at 3 to 5%, barely above cold outreach. The lesson: the strength of your connector's relationship with the investor matters more than the strength of your relationship with the connector.

SaaStr founder Jason Lemkin has made a related point from the investor side: 90% of warm intros are a waste of time unless they are "double qualified," meaning the connector actually understands what makes a good venture investment and has vetted the fit between the founder and the specific investor's thesis. A well-meaning friend who has no context on the VC's portfolio strategy is not delivering a warm intro. They are delivering a slightly warmer cold email.

Map Your Introduction Paths Before You Need Them

The single biggest mistake founders make is treating introductions as a fundraising activity. They are a pre-fundraising activity. Start 10 to 12 weeks before you need capital, not when you are already running a process.

Begin by building your target investor list. Identify 30 to 50 investors who are a genuine thesis fit, not just any VC with a checkbook. For each investor, map the introduction path on LinkedIn: who in your network has a first-degree connection to them? Prioritize connectors in this order:

1. Portfolio founders of the target fund (highest conversion, highest signal).

2. Your own existing investors and advisors (they have financial incentive to help you raise).

3. Other founders who have recently fundraised and met with the target investor.

4. Industry professionals, lawyers, or accountants who work with that VC's portfolio companies.

If you cannot find a warm path to an investor, that is useful information. It either means the investor is outside your ecosystem (and probably not a fit), or you need to invest time building the relationship before making the ask. Attend the events they attend. Comment thoughtfully on their content. Build familiarity before you need anything.

Use Double Opt-In, Every Time

In 2009, Fred Wilson, co-founder of Union Square Ventures, proposed a simple practice he called the "double opt-in introduction". The concept: before connecting two people who do not know each other, the intermediary checks with both sides first. If either says no, the introduction does not happen.

This practice is now near-religious in Silicon Valley. Its rapid adoption reflects a deeper truth about venture capital: the two most prized resources in the industry are time and personal networks. A forced introduction wastes both.

For founders, this means never asking a connector to send a blind CC introduction. Instead, ask them: "Would you be comfortable checking with [Investor] whether they are open to an intro?" Send your connector everything they need to make the ask easy, which brings us to the most important asset in your fundraising toolkit.

Write a Forwardable Blurb That Does the Work

The forwardable blurb is the single most underused tool in fundraising. It is a short, self-contained description of your company that your connector can paste into an email and hit send. Eric Bahn, co-founder of Hustle Fund, uses forwardable blurbs nearly a dozen times a day. It is one reason Hustle Fund raised $46.1 million for their third fund.

A strong blurb is under 120 words. It covers four things: what you do (one sentence), your strongest traction proof point, why this specific investor is a fit, and a link to your deck. That is it. No vision statements. No market sizing. No three-paragraph founder backstory.

Here is the formula that works:

[Company name] is [one-line description]. We are at [traction metric, e.g., $200K ARR growing 15% MoM, 50 enterprise customers, 10x retention vs. industry average]. We are raising a [$X round] and [Investor Name] is a strong fit because [specific reason tied to their thesis or portfolio]. Deck attached.

The key principle, as multiple operator guides emphasize: make it effortless for the person doing you the favor. The more your connector has to think and write, the less likely the intro actually happens. Providing a forwardable blurb can double the chances of getting the introduction made.

Timing and Sequencing: How to Run the Intro Campaign

Timing matters more than most founders realize. Founders who begin building intro paths six or more months before their raise close at higher valuations, because they enter the process with momentum rather than desperation.

Do not ask one connector to make 10 introductions. Focus on their two or three strongest connections, the ones where they have real social capital. A request for one well-targeted intro signals respect for the connector's network. A request for a dozen signals that you have not done your homework.

After the intro is made, your follow-up cadence matters as much as the intro itself. Respond within 24 to 48 hours. If the investor does not respond within a week, send one gentle follow-up to your connector asking whether they have heard back. If nothing materializes after a second gentle nudge, move on without burning the relationship. Some people agree to introductions they are not actually comfortable making. Accept that and maintain enough parallel paths that one stalled intro does not derail your timeline.

One caveat that seed-stage investors evaluate differently than Series A leads: at seed, a strong narrative and founder credibility can carry the meeting. At Series A and beyond, VCs will expect the intro to come paired with hard metrics. Adjust your blurb accordingly.

What If You Do Not Have a Network Yet?

This is the hardest question in fundraising, and the most common one from first-time founders. The honest answer: it takes time, but there are accelerated paths.

Accelerator programs remain the fastest network hack. Y Combinator alumni raise follow-on funding at significantly higher rates and valuations than comparable non-YC startups, largely because the alumni network provides warm introductions that would take years to build organically. Programs like Techstars, 500 Global, and On Deck have similar (if smaller) effects.

Outside of accelerators, the playbook is straightforward but requires consistency. Meet other founders who are six to twelve months ahead of you in their fundraising journey. Attend investor-facing events, not to pitch, but to build genuine relationships. Publish your thinking on LinkedIn or in founder communities. Ask for advice calls, not investment calls. Over time, the advisors and founders you build relationships with become the connectors who make introductions on your behalf.

There is a structural inequity here worth acknowledging. Founders from underrepresented backgrounds, those without elite university networks or existing connections to the VC ecosystem, face a steeper path to warm introductions. This is a real problem the industry has not solved. Research shows that 40% of all VCs went to just two schools, which creates significant network overlap and limits access for outsiders. Working with fundraising advisory firms, joining diverse founder communities, and targeting investors who explicitly source outside their networks can help mitigate this gap.

Five Mistakes That Kill Warm Introductions

After working with over 1,300 founders through the capital readiness process, we see the same patterns repeatedly:

1. Asking for the intro before the relationship is warm enough. If you met someone at a conference once and never followed up, you do not have a warm connection. You have a LinkedIn contact.

2. Sending the blurb through the wrong channel. Sharing your forwardable blurb via WhatsApp or Telegram instead of email makes it harder for the connector to forward it professionally.

3. Writing a blurb that is too long. If your company description exceeds 250 words, no one will forward it. Keep it under 120.

4. Not responding quickly once the intro is made. Investors form impressions fast. DocSend data shows investors spend 2 to 3 minutes on a first-pass deck review. If you take a week to reply to an introduction, you have already lost.

5. Failing to thank the connector. Whether the intro converts or not, close the loop. A connector who feels appreciated will make introductions again. One who feels used will not.

The Introduction Is the Beginning, Not the End

A warm introduction gets you in the room. It does not close the deal. Once you are there, the quality of your deal, your narrative, your metrics, and your ability to withstand diligence scrutiny is what determines the outcome.

What we see across hundreds of fundraising processes at Funden is that the founders who raise successfully are not the ones with the most introductions. They are the ones who go to market with an institutionalized deal, a stress-tested narrative, and a clear understanding of how investors will evaluate them. The introduction is a door. What you bring through it is what matters.

If you are preparing for a raise and want structured feedback on your deal before going to market, Funden works with founders to pressure-test their narrative, benchmark their round, and make targeted introductions to our network of 1,000+ partner funds. Apply at funden.com.

B2B SaaS Fundraising in 2026: What Actually Works When Capital Is Selective

Nearly $48 billion flowed into U.S. venture funds in Q1 2026 alone, per PitchBook and NVCA data reported by Axios. That is more capital raised in a single quarter than in all of 2025 combined.

Nearly $48 billion flowed into U.S. venture funds in Q1 2026 alone, per PitchBook and NVCA data reported by Axios. That is more capital raised in a single quarter than in all of 2025 combined. But here is the number that matters more for B2B SaaS founders: the top five fund closes accounted for over $35 billion of that total. Capital is back. It is just not evenly distributed.

For founders building subscription software businesses, this bifurcation changes the playbook. The strategies that worked in 2021, when investors wrote checks on TAM slides and triple-digit growth projections, are not the same strategies that close rounds today. What follows is a data-driven breakdown of how B2B SaaS founders should approach fundraising in the current market, from the metrics investors actually care about to the timing and structural decisions that separate successful raises from stalled ones.

The Market Has Split. Your Strategy Should Too.

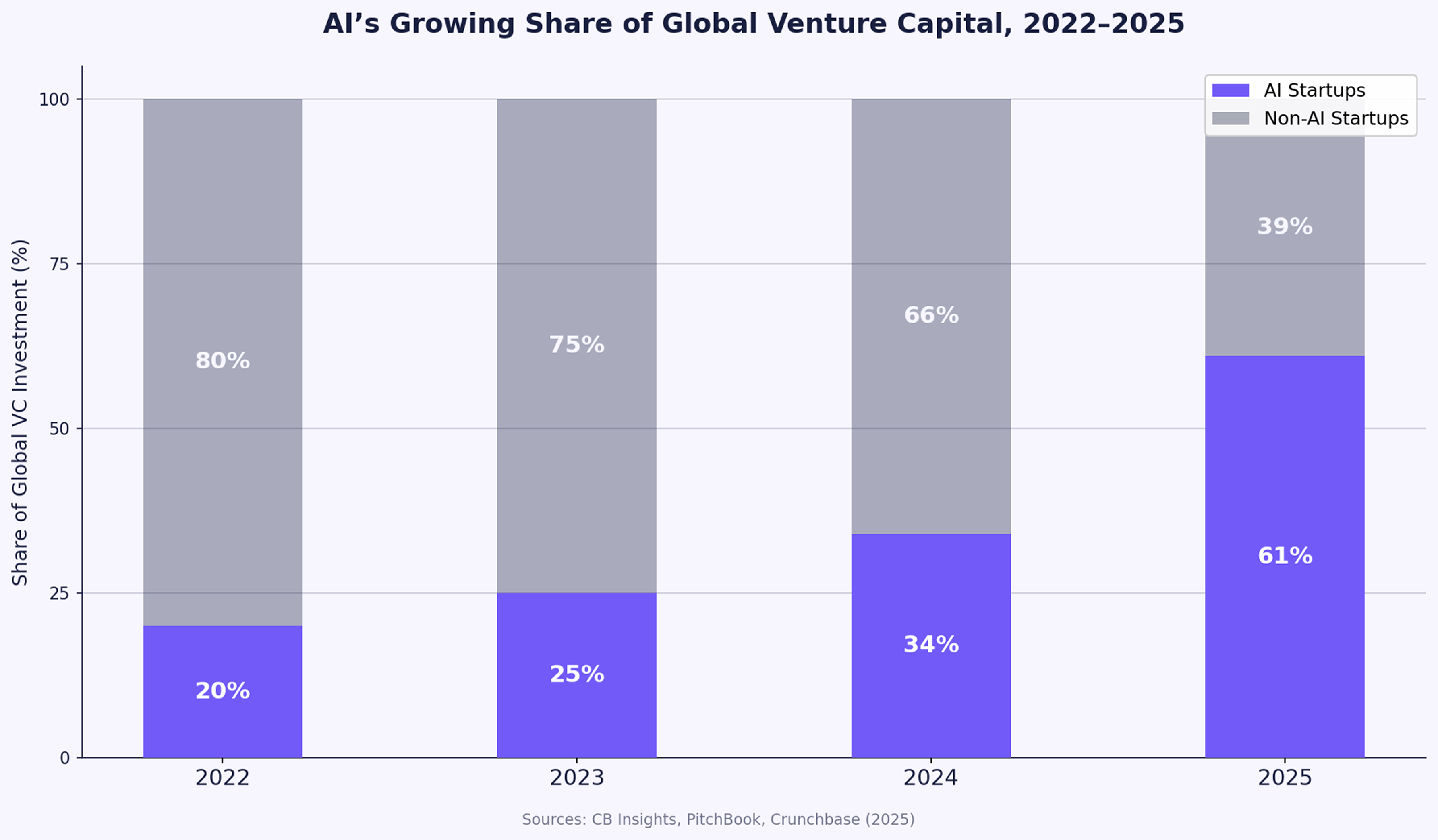

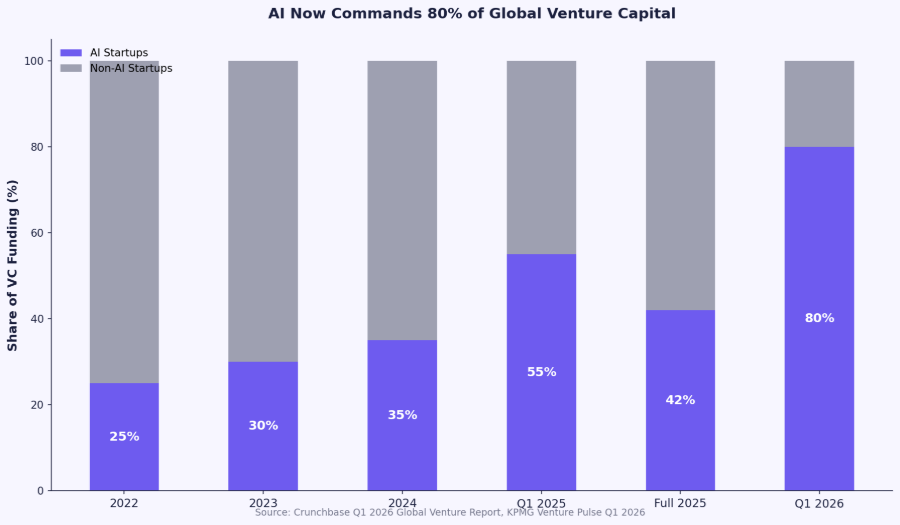

AI startups captured 61% of all global venture investment in 2025, totaling roughly $258 billion out of $425 billion deployed worldwide. Wellington Management's 2026 outlook described the market as "bifurcated," with AI-driven companies attracting capital while most others face tighter purse strings.

This does not mean non-AI B2B SaaS is unfundable. It means the bar has moved. Investors who once underwrote growth potential now underwrite growth proof. According to Carta's Q4 2025 data, the median post-money valuation at seed hit $24 million, up from $18 million a year earlier. At Series A, the median reached $78.7 million, up 37% year over year. Fewer deals are getting done, but the founders who do close are raising at record prices.

The practical implication: if you are building B2B SaaS and you are not in the AI mega-round category, you need a fundraising approach that is more precise, better timed, and more metrics-driven than what worked even 18 months ago.

What Investors Actually Underwrite in B2B SaaS Right Now

The metrics conversation has shifted. During the 2020 to 2021 boom, a SaaS company could raise a Series A with under $1 million in ARR if the narrative was strong enough. That threshold has risen significantly. Most Series A investors now expect $2 million to $5 million in ARR with healthy gross margins and clear retention signals, according to Carta and multiple institutional VCs surveyed by Crunchbase.

Private SaaS valuation multiples reflect this discipline. SaaS Capital's index shows bootstrapped B2B SaaS companies trading at around 4.8x ARR, while equity-backed companies average 5.3x. High-growth outliers with strong net revenue retention above 110% and Rule of 40 scores above 50 can still reach 7x to 10x. But the median is the median for a reason. Most companies land in the 4x to 6x range.

What this means for founders: before you start pitching, stress-test your metrics against the benchmarks investors actually use. The three numbers that move the needle most are ARR growth rate, net revenue retention, and gross margin. If you are growing at 30% or more with NRR above 110% and gross margins above 70%, you are in the conversation. Below those thresholds, you will need a compelling reason for why those numbers are about to change, backed by evidence, not projections.

One caveat that matters at the seed stage: 92% of pre-seed rounds now use post-money SAFEs rather than priced equity, per Carta's State of Seed report. The median post-money SAFE valuation cap at seed sits around $20 million. If your cap is well above that median without the traction to justify it, expect a harder conversation with follow-on investors at your Series A.

Build Your Fundraise Around Runway, Not Speed

High Alpha's SaaS benchmarks show that 47% of B2B SaaS founders spent four to six months actively raising their most recent round. Another 14% took seven to twelve months. Only 8% closed in under a month. The median time between seed and Series A has stretched to 18 to 24 months, up from 12 to 14 months in 2021, per Value Add VC's analysis of Carta and PitchBook data.

The conversion rate from seed to Series A has also compressed. It has dropped from roughly 50% to around 38% across the market. At Series B, the picture is even tighter. Only about 9% of Series A companies on Carta secured Series B funding within two years, a sharp decline from the previous rate of 25%, according to TechCrunch's reporting on Carta data.

The founders who handle this well are the ones who plan for it before they need to. Raise enough to give yourself 18 to 24 months of runway, not 12. Build your financial model around the assumption that your next round takes six months to close, not three. And start relationship-building with your next-stage investors at least 12 months before you plan to raise, especially at Series B, where cold inbound is far less effective than at earlier stages.

The Narrative Gap Most B2B SaaS Founders Miss

Metrics get you in the door. Narrative gets you the term sheet. In a market where investors are reviewing fewer deals but spending more time on each one, the quality of your fundraising story matters more than it did when checks were moving fast.

The most common narrative gap we see across hundreds of fundraising processes at Funden: founders lead with what their product does instead of what problem it solves at scale. Investors in 2026 want to know why your category is large, why existing solutions fail, why your go-to-market motion compounds over time, and why now. The "why now" is especially important in B2B SaaS, where many categories feel crowded. The best fundraising decks we see frame the timing around a structural shift, not just a product launch.

SG Analytics noted in their 2026 US VC outlook that AI startups raise capital earlier and faster, with a median age at first financing 65% lower than non-AI peers. If you are not in the AI category, you need to work harder to create that same sense of urgency. The way to do it is through specificity: specific customer wins, specific retention cohorts, specific competitive differentiation that an investor can verify in two phone calls to your customers.

Match Your Round Structure to the Market

Round structure decisions are strategic, not administrative. The market has several nuances worth planning around.

At pre-seed and seed, SAFEs remain the dominant instrument. But founders should be intentional about their valuation cap. Carta's pre-seed data shows median SAFE caps of $10 million for rounds under $1 million and $15 million for rounds in the $1 million to $2.5 million range. Setting your cap too high relative to your traction creates a signaling problem when Series A investors start their due diligence.

At Series A and B, the conversation is different. Dilution at Series A has settled at around 17% to 20%, per Carta. The founders who get better terms are not necessarily the ones with the highest ARR. They are the ones who create competitive dynamics in their process. That means running a structured fundraise with a defined timeline, clear materials, and enough investor conversations happening in parallel that no single firm has unilateral pricing power over your round.

For later-stage B2B SaaS companies considering a raise in 2026, Crunchbase data shows the Series B pipeline is diversifying, with healthcare, biotech, and vertical SaaS attracting meaningful capital alongside AI. The average Series B has reached $68 million so far this year, the highest on record. But smaller Series B rounds under $10 million are becoming rare, with only 44 such deals in 2025 compared to 150 per year from 2020 to 2023.

The Capital Efficiency Signal Investors Cannot Ignore

One of the strongest signals a B2B SaaS founder can send in 2026 is capital efficiency. Pilot's proprietary data shows that 24% of unprofitable, venture-backed companies now have more than 36 months of runway, up from 18% in 2023. Companies that extend their runway while maintaining growth are rewarded with better terms because they demonstrate the discipline investors now prioritize.

Average seed-stage team sizes have dropped to 6.2 equity-holding employees, down from 10.3 at the 2021 peak, per Carta and a16z's speedrun analysis. Hiring has slowed to its lowest rate since before 2019. This is not a sign of weakness. It reflects a structural shift where founders are building more with smaller teams, partly enabled by AI tooling, and investors are rewarding it. If you can show $2 million in ARR with a team of six, that tells a very different story than $2 million with a team of twenty.

Raise Like the Market Has Changed, Because It Has

The B2B SaaS fundraising environment in 2026 is not hostile. It is selective. Capital is flowing, valuations are at record levels for the companies that earn them, and investors are actively looking for strong SaaS businesses outside of the AI mega-round category. But the margin for error is thinner. Founders who treat fundraising as a structured, metrics-driven process, who build investor relationships early, who stress-test their narrative before going to market, are the ones closing rounds at favorable terms.

That is exactly what Funden helps founders do. We work with B2B SaaS companies to institutionalize their deal, pressure-test their positioning with real market feedback, and connect them with the right investors before the first pitch. If you are preparing for a raise and want structured, honest feedback on your deal before going to market, apply at funden.com.

Why Founders Fail at Raising Capital (And What the Data Says They Get Wrong)

Roughly 75% of venture-backed startups never return capital to their investors, according to research from Harvard Business School. That number has held steady for years, even as the total pool of venture capital has exploded.

In Q1 2026, global VC investment hit $330.9 billion, more than doubling the prior quarter. That single quarter outpaced every full year of venture spending before 2019. The money is there. It has never been more plentiful.

So why do so many founders still walk away empty-handed?

The answer, based on data from hundreds of post-mortems and thousands of fundraising processes, is not that capital dried up. It is that founders consistently make the same correctable mistakes before, during, and after their raise. This piece breaks down what those mistakes actually are, why they persist, and what the founders who close their rounds do differently.

The Capital Is There. Access to It Isn’t.

$330.9 billion sounds like every founder should be able to raise. The reality is much more concentrated than the headline suggests.

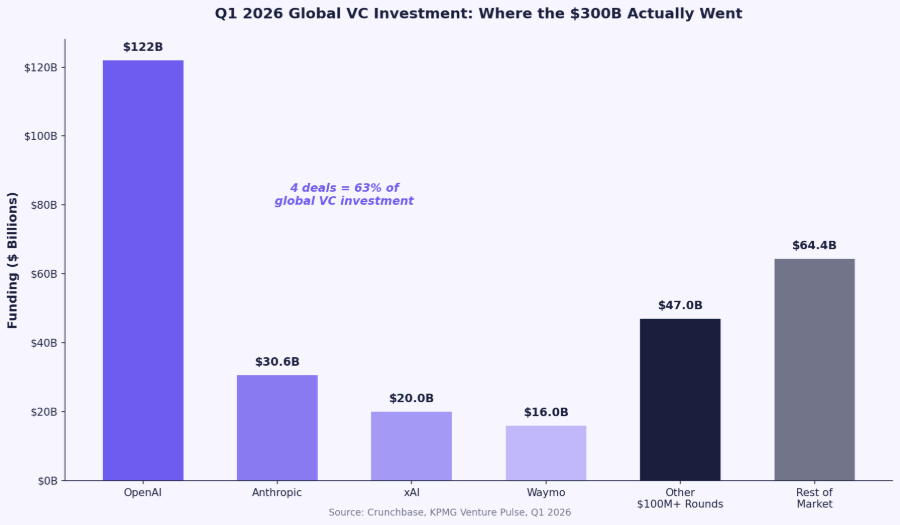

Four mega-deals in Q1 2026 accounted for the vast majority of total capital. OpenAI ($122B), Anthropic ($30B), xAI ($20B), and Waymo ($16B) collectively raised $188 billion, roughly 57% of the global total. Another $47 billion went to 154 additional late-stage companies raising $100M+. That leaves early-stage founders splitting $41.3 billion across 1,800 deals, and seed founders splitting just $12 billion.

Source: Crunchbase, KPMG Venture Pulse, Q1 2026

Seed deal counts fell 30% year over year even as total seed dollars rose 31%. The increase came entirely from larger individual rounds, not from more founders getting funded. In other words, fewer founders are raising, but the ones who do are raising bigger checks. The bottom 50% of startups on Carta that closed a round in 2025 combined to bring in just 14% of all cash raised. The top 10% captured roughly half.

This is the market every founder walks into. The money exists. The bar to access it has never been higher.

Mistake #1: No Product-Market Fit, No Honesty About It

42% of startups that fail cite a lack of market demand as the primary cause, according to CB Insights analysis of 110+ post-mortems. That number has been consistent for years. It remains the single most common reason companies shut down.

A 2026 survey of 200 U.S. tech founders by Wilbur Labs found that 54% named understanding product-market fit as the most important lesson they learned from failure. Interestingly, fewer founders in 2026 blamed running out of money (25%, down from 38% in 2023). The most-cited cause shifted to technology or product issues at 44%.

What does this mean for fundraising? Investors have recalibrated accordingly. In 2026, many seed investors expect $300K to $500K in ARR before writing a check, according to Pitchwise benchmarks. That would have been a Series A expectation a few years ago. The seed stage now looks like what Series A used to be.

The caveat here: this benchmark skews toward U.S.-based software companies. International founders, hardware startups, and biotech companies face different thresholds. But the direction is clear. Showing up with a concept and a TAM slide is no longer sufficient at any stage.

Source: CB Insights (110+ post-mortems), Wilbur Labs 2026 Survey (200 founders)

Mistake #2: Going to Market Too Early

616 days. That is the average time between a seed round and a Series A round in 2026, per Pitchwise data. Investors are not penalizing founders for taking longer. They are penalizing founders for raising too early with thin metrics.

This is one of the most expensive mistakes in fundraising, and we see it repeatedly across hundreds of processes at Funden. A founder goes to market before their numbers are ready. They take 40 to 60 meetings. Most investors pass. Now the founder has burned through their best investor relationships, and the signal in the market is negative. Rebuilding momentum from that position is significantly harder than waiting three more months to hit the right milestones.

The median post-money valuation at seed has climbed to $24 million as of Q4 2025, up from $18 million a year prior and $16 million the year before that. Higher valuations mean higher expectations. A $24M post-money valuation on a $4M seed round implies the investor expects massive growth to justify a strong Series A step-up. Founders who raise at these valuations without the underlying traction are setting themselves up for a painful next round.

Source: Carta State of Private Markets, 2020-2025

Mistake #3: A Pitch Deck That Doesn’t Survive the Two-Minute Test

The average investor spends roughly 2 to 3 minutes reviewing a pitch deck, according to DocSend data. For seed-stage decks, that number drops even lower. And only 58% of pitch decks are viewed to completion. Nearly half of founders lose investor attention before reaching their final slides.

The slides that pull the most viewing time are not the ones most founders obsess over. Investors linger on the team slide, the financials slide, and the "why now" slide. Product slides, ironically, get the least time because investors process visual product screenshots quickly. The practical implication: if your business model, financials, and team composition are not crystal clear within the first few slides, the rest of the deck may never get read.

DocSend's research also shows a weak correlation between the number of investors contacted and meetings held. Reaching out to more VCs does not reliably produce more meetings. Reaching the right VCs, with a deck optimized for how they actually consume information, produces meetings. Spray-and-pray outreach is one of the most common time sinks in early-stage fundraising.

Mistake #4: Financial Illiteracy at the Wrong Moment

In 2026, financial discipline is no longer a Series B concern. It is a seed-stage expectation.

A burn multiple under 2x is the baseline expectation at most stages, meaning net burn should be less than twice net new ARR. Top-performing startups in the current environment operate between 1x and 1.5x. Runway of more than 18 months at current burn is the minimum that gives founders genuine negotiating leverage. Below that, the power dynamic shifts decisively toward the investor.

Series A teams now average 16.8 employees, down from 25.9 in 2021. Series B teams average 48.2, down from 72.3 in 2022. AI has accelerated this shift. Smaller teams, same outcomes. Investors notice when a seed-stage company has 20 people and a burn rate that assumes perpetual funding. The founders who close in this market are the ones who can demonstrate how every dollar gets deployed and what measurable milestone it funds.

If you cannot clearly articulate your CAC payback period, your LTV/CAC ratio, or your path to positive unit economics at the unit level, investors in 2026 will move on. These are no longer Series A questions. They are seed questions.

Mistake #5: Treating Fundraising as a Side Project

The founders who fail at raising capital often treat the process like networking: send the deck to 50 investors, take meetings as they come, and hope someone bites. The founders who close treat it like a structured deal execution.

What does that look like in practice? The strongest raises in 2026 follow a pattern. The founder has a data room ready before the first investor meeting, not after. In 2026, many investors expect a data room almost immediately after reviewing the deck, sometimes right after the first call. A well-organized data room signals operational maturity and transparency. It also accelerates diligence.

The founder has also built investor relationships months before opening the round. The strongest position you can be in when raising is one where you genuinely do not need the money to survive. That posture changes every conversation. Investors can sense when capital is existential, and they price that desperation into the terms.

46% of all seed transactions in Q1 2025 were bridge rounds, per Carta data, the highest proportion ever recorded. That tells you how many founders are running out of runway and raising from a position of weakness. It does not have to work this way.

What Founders Who Close Actually Do Differently

The pattern across founders who successfully raise in this market is consistent, even if their companies look very different.

They are "default alive" before they start the process. Their company will reach profitability on existing revenue and cash without needing additional funding. The raise is for acceleration, not survival. That distinction changes every conversation.

They pressure-test the deal before going to market. They get structured feedback on their narrative, positioning, and deal structure from people who evaluate deals for a living. Not from advisors who tell them what they want to hear. Not from fellow founders who lack the investor lens. From the market itself.

They target investors with precision. A founder who sends 100 cold emails to generalist VCs will get fewer meetings than one who sends 20 warm introductions to investors who have a published thesis in the founder's vertical and stage. This is where most spray-and-pray outreach breaks down. Volume does not compensate for fit.

And they have a clear "why now" that connects to macro market forces. Investors in 2026 are increasingly focused on what some have called "high-context founders": people with deep domain expertise who know their customer before they have even built the product. AI has commoditized the ability to write code and build prototypes. The competitive edge now sits in distribution, domain knowledge, and founder-market fit.

The Raise Starts Before the Raise

The common thread across every failed raise is not bad luck or a bad market. It is inadequate preparation. Founders who lose their raise almost always went to market too early, with too little traction, an unclear narrative, or no structured process.

The market in 2026 rewards discipline more than any market before it. Fewer deals are getting done. The ones that close are better prepared, better targeted, and better structured than the average pitch that lands in an investor's inbox.

Most founders don't fail because investors say no. They fail because no one tells them the truth early enough. That is what Funden does. We work with founders to institutionalize their deal, stress-test it with real market feedback, and target the right investors with the right narrative. If you are preparing for a raise and want structured feedback before going to market, apply at funden.com.

$300 Billion in One Quarter: What Q1 2026 Actually Means for Founders Raising Capital

Investors poured $300 billion into startups globally in Q1 2026, according to Crunchbase.

Investors poured $300 billion into startups globally in Q1 2026, according to Crunchbase. That single quarter topped every full year of venture activity before 2019. Headlines called it a record. Venture Twitter celebrated. But the number tells a misleading story.

Four deals accounted for $188 billion of that total. OpenAI ($122 billion), Anthropic ($30 billion), xAI ($20 billion), and Waymo ($16 billion). Strip those out, and Q1 looks a lot more like a normal market. For founders raising seed or Series A rounds, the $300 billion headline is noise. The signal is in the details underneath it.

The Concentration Problem Is Getting Worse, Not Better

KPMG's Venture Pulse report puts the Q1 figure even higher at $330.9 billion. Either way, the story is the same: ten funding rounds of $2 billion or more contributed over $206 billion to the global total. The U.S. alone absorbed $267 billion, more than double its previous quarterly record.

This concentration is not new, but it has accelerated sharply. Crunchbase data shows that over 40% of all seed and Series A investment in 2026 has gone to rounds of $100 million or more. That figure was negligible five years ago.

Carta's 2025 year-in-review found that the bottom 50% of U.S. startups that closed a round combined to bring in just 14% of all capital raised. The top 10% took roughly half. Total round count on the platform fell to a six-year low, even as total dollars invested grew 17% year over year to nearly $120 billion.

That means fewer founders are getting funded. But those who do are raising larger amounts at higher valuations. The spray-and-pray era is definitively over.

What the Seed Market Actually Looks Like Right Now

$12 billion went to seed-stage startups globally in Q1 2026, per Crunchbase. That is up 31% year over year. Sounds healthy. But deal counts dropped 30% to 3,800. More money flowing into fewer companies.

Carta reported that the median seed post-money valuation hit $24 million in Q4 2025, a new all-time high. A year earlier it was $18 million. Two years before that, $16 million. At Series A, the median climbed to $78.7 million, up 37% year over year.

The valuation increase is not driven by bigger check sizes. Median seed deal size has held steady at $3 million for six of the past seven quarters. Instead, dilution is declining. Median dilution across seed through Series C fell from about 18% to 16% over the past year, per Carta. Founders who can raise are keeping more of their companies. Founders who cannot raise are not part of these numbers at all.

46% of seed-stage transactions in Q1 2025 were bridge rounds, the highest proportion ever recorded. That stat, from Carta's State of Seed report, tells you what life looks like for the majority of seed-funded companies: they are extending runway, not stepping up to a priced Series A. The bridge round has become the default path for startups that are growing but not fast enough to clear today's bar.

AI Is Pulling Capital Away from Everything Else

80% of all global venture funding in Q1 2026 went to AI companies, per Crunchbase. The previous record was 55%, set just one year earlier. Seven of the ten largest deals in the quarter were U.S.-based AI companies.

Carta's 2025 review showed that at Series A, the median AI startup valuation was 38% higher than the median non-AI valuation. At Series E and beyond, the AI premium reached 193%. At the seed stage, AI companies command roughly a 42% valuation premium over non-AI peers.

For non-AI founders, this creates a real but manageable challenge. Investors are not ignoring non-AI deals. They are just writing fewer, higher-conviction checks. If you are building in SaaS, fintech, healthtech, or any sector outside AI infrastructure, the fundraising bar is higher than it was 18 months ago. You need stronger unit economics, clearer differentiation, and a tighter narrative. What you don't need is to bolt an AI story onto your pitch that does not belong there. Investors can spot that immediately.

Valuations Are Up. Deal Counts Are Down. Both Things Matter.

This is the dynamic that defines the current market. Carta's data shows that at both the 25th percentile and 75th percentile, seed and Series A valuations are rising to all-time highs. The broad uplift means this is not just a top-of-market phenomenon. Even middle-tier deals are pricing higher.

But the bar for getting a deal done at all keeps rising. Fewer than 14% of new fundings on Carta in Q4 2025 were down rounds, the lowest rate in three years. That sounds positive until you realize the denominator has shrunk. The companies that could not raise at all do not appear in the down-round stats. They simply disappeared from the data set.

For founders preparing to raise, this means two things. First, if your metrics clear the bar, you will likely raise at favorable terms. VCs are competing to deploy into their highest-conviction bets, which pushes valuations up and dilution down. Second, if your metrics do not clear the bar, you may not get a term sheet at all. The middle ground, where a mediocre startup could still close a round on acceptable terms, has largely evaporated.

The IPO Backlog Creates Downstream Pressure

200 to 230 IPOs are expected in 2026, raising between $40 billion and $60 billion, according to Renaissance Capital. SpaceX, OpenAI, Anthropic, Databricks, Canva, and Stripe are all in various stages of IPO preparation. If even a few of these go public, it would unlock significant LP liquidity that flows back into venture funds.

This matters for early-stage founders because the VC capital cycle is a pipeline. When LPs get cash back from exits, they re-commit to funds. When funds raise successfully (and Q1 2026 saw $47.8 billion in new U.S. fund commitments, already more than half of 2025's full-year total), that capital eventually gets deployed into seed and Series A deals. The IPO window opening is a trailing indicator that the early-stage funding environment should continue to improve through the rest of 2026.

What This Means for Your Fundraise

Time your raise around your metrics, not around market headlines. The market is strong, but it rewards preparedness. Going out too early with weak metrics wastes your one shot at first impressions with the investors who matter most.

Expect longer timelines if you are outside AI. Non-AI startups are closing rounds, but VCs are taking more meetings and doing more diligence before committing. Build your pipeline wider and start earlier than you think you need to.

Anchor your valuation expectations in data, not in headlines. The $300 billion number includes rounds that have nothing to do with your market. Use Carta benchmarks and comparable recent rounds in your sector to set realistic expectations. A $24 million median seed valuation does not mean every seed company is worth $24 million.

Treat your deal like an institutional product. Investors are writing fewer, larger checks. They want to see an institutional-grade opportunity with a clear risk framing, a defensible narrative, and a data room that holds up under scrutiny. The bar for deal quality has never been higher.

Conclusion

The $300 billion headline is real, but the market underneath it is more nuanced than any single number can capture. Capital is abundant for the right companies and functionally scarce for everyone else. Valuations are at all-time highs, but deal counts are at multi-year lows. AI dominates the funding conversation, but strong non-AI companies are still raising.

For founders, the takeaway is not to chase the moment. It is to prepare for it. The founders who perform best in this market are the ones who go to market with a deal that has been pressure-tested: a narrative that holds up against investor scrutiny, metrics that match or exceed the benchmarks, and a process that treats fundraising as a structured campaign rather than a series of hopeful intro emails.

That is what Funden does. We work with founders to institutionalize their deal before it hits the market, so the first impression with investors is the right one. If you are preparing for a raise and want structured feedback from people who have supported 1,300+ founders through this process, apply at funden.com.

Get our notes on capital-readiness before the round opens.

A monthly email from the Funden team — market structure, narrative craft, and what investors are actually underwriting right now. Sent the first Monday of every month. Two minutes to read. No noise.

Join 4,000+ founders, operators and investors who read it every month.

One email a month. Unsubscribe any time. We never share your address.