Fundraising Ideas in 2026: What Actually Works Now

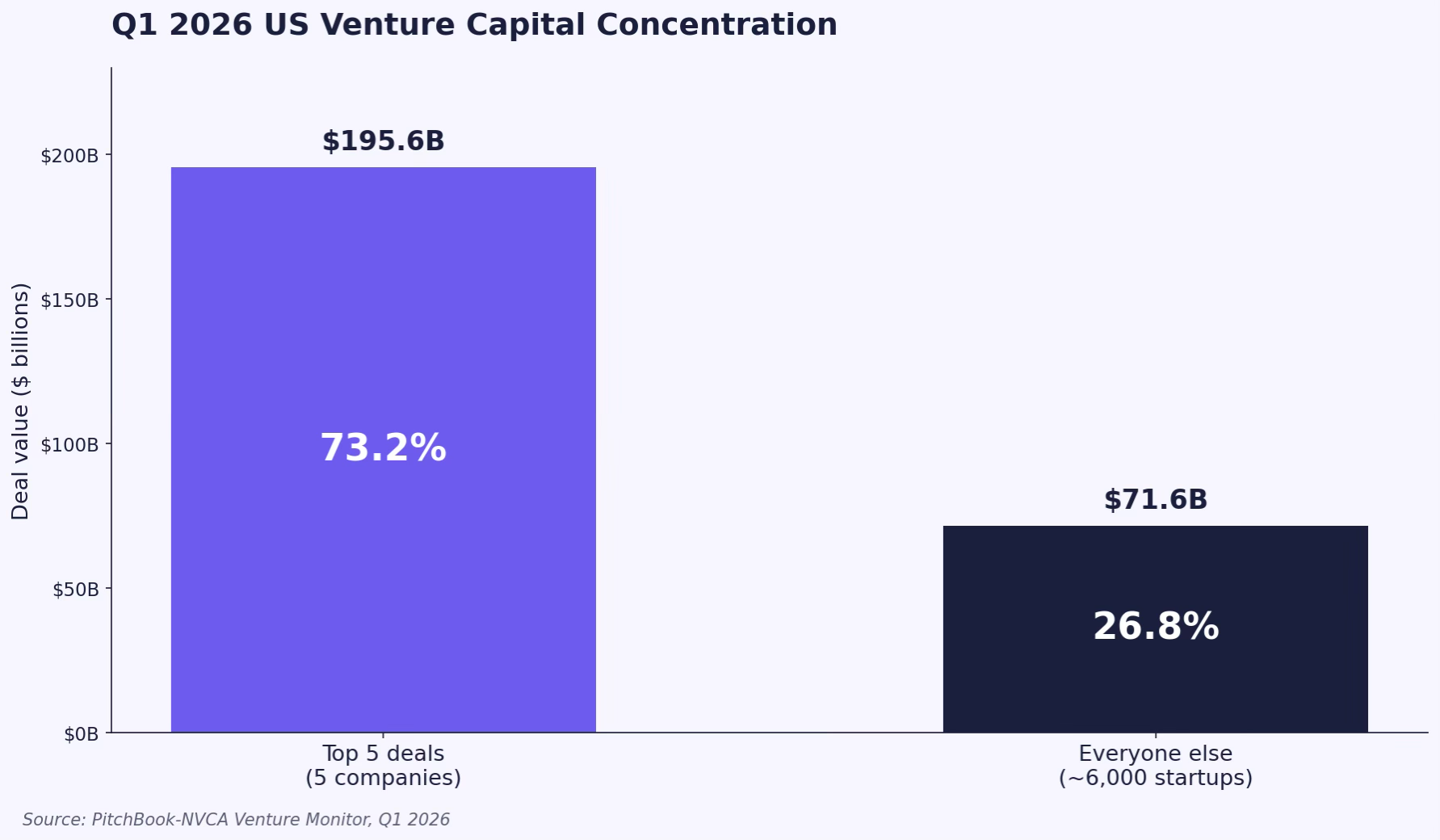

In Q1 2026, US startups raised $267.2 billion. Five companies took roughly three-quarters of it. According to the PitchBook-NVCA Venture Monitor, remove the top five deals and quarterly venture funding falls 73.2%. The headline numbers look like 2021 came back. Underneath, the experience for most founders is closer to 2023.

If you are not OpenAI, Anthropic, xAI, Waymo, or one of the handful of frontier labs absorbing sovereign-scale checks, your raise in 2026 is going to look more like a long, structured search than a competitive auction. Median time between a seed and Series A reached 616 days, more than 20 months, according to Carta. SVB summarised the dynamic plainly in its H1 2026 State of the Markets: the venture market is bifurcated, with abundance at the apex and measured scarcity elsewhere.

What follows is not a generic list of fundraising tips. These are seven strategies we see closing rounds right now, drawn from current investor behaviour and from the patterns we observe working with founders preparing to go to market. If you are in the 99% of founders not raising on the strength of being a frontier model, this is the playbook that fits the actual market you are raising into.

1. Build a deal investors can underwrite, not a story you can pitch

The most common mistake in 2026 is treating fundraising like a marketing exercise. Founders polish the deck, rehearse the story, build a target list, and start emailing. Three months later they have a pile of soft passes and no idea why.

The reason is structural. With $255.5 billion of AI capital deployed in a single quarter and most of it concentrated in fewer than ten companies, partners at non-AI-focused funds are under pressure to make every check count. A clean narrative is no longer enough. Investors are underwriting deals the way an acquirer would: looking at unit economics, retention, defensibility, team composition, capital efficiency, and exit pathways before they decide a meeting is worth taking.

Treat your raise like an institutional transaction from day one. Before you build the deck, write the investor memo. Stress-test the financials. Identify the three objections any sharp partner will raise and prepare for them with data, not adjectives. The founders we see closing rounds in 2026 spend longer preparing and less time pitching. That ratio is almost always inverted in struggling raises.

A useful caveat: this advice applies to priced rounds and any SAFE above roughly $1.5M. For a $500K friends-and-family note from people who already believe in you, the deal-readiness work matters less. For everything else, it is the work.

2. Run the round like a search for one lead, not a poll of 100 maybes

Spray-and-pray outreach to 200 funds is a comfort behaviour. It feels productive. It rarely closes a round. The mechanics of a priced round still require a lead investor willing to set terms, write the largest check, and pull the rest of the syndicate along. Until you have a lead, you do not have momentum, no matter how many partner meetings you take.

DocSend's pitch deck research has consistently found that decks resulting in a meeting average about three and a half minutes of investor reading time, and that the correlation between number of investors contacted and dollars raised is weak. Reaching the right ten investors matters more than spraying 200.

Build a short list of 30 to 50 funds whose thesis, stage, and check size actually match your round. Within that list, identify five to ten potential leads. Sequence your outreach so the most likely leads are not the first conversations. Open with two or three investors whose feedback you respect but who are unlikely to lead, use those meetings to pressure-test the pitch, then move into the lead conversations once the narrative is sharp.

Run parallel processes. A lead investor will move faster if they sense competitive tension, even if that tension comes from one credible alternative rather than five. Sequencing is not deceptive, it is professional.

3. Engineer warm intro paths 90 days before you open the round

Cold outreach response rates to investors sit around 3 to 5%. Warm intros from a trusted source pull that into the 15 to 20% range. The math is straightforward, and yet most founders treat the warm-intro problem as something to solve once fundraising has started. By then, it is already too late.

Map your target investor list to your existing network roughly 90 days before you plan to open the round. For each fund on the list, identify two to three credible introduction paths: a portfolio founder, a co-investor at a previous round, an angel they trust, an operator they have backed. Most founders find they already have one or two paths into 60% of their list. The remaining 40% requires deliberate relationship building, which is the work that needs the 90-day runway.

The intro path matters as much as the existence of an intro. A passing forward from someone who barely knows you signals nothing. An intro from a portfolio founder who can speak to specifics about your team or product is a different document entirely. The strongest signal is what the warm-intro literature calls a hot intro: the connector is putting their own check in. That is the version that closes seed rounds.

If you do not have those paths yet, the 90 days before you raise are when you build them. Show up in the conversations the people you want intros from are actually in. Help before you ask.

4. Stack non-dilutive capital before you sell equity

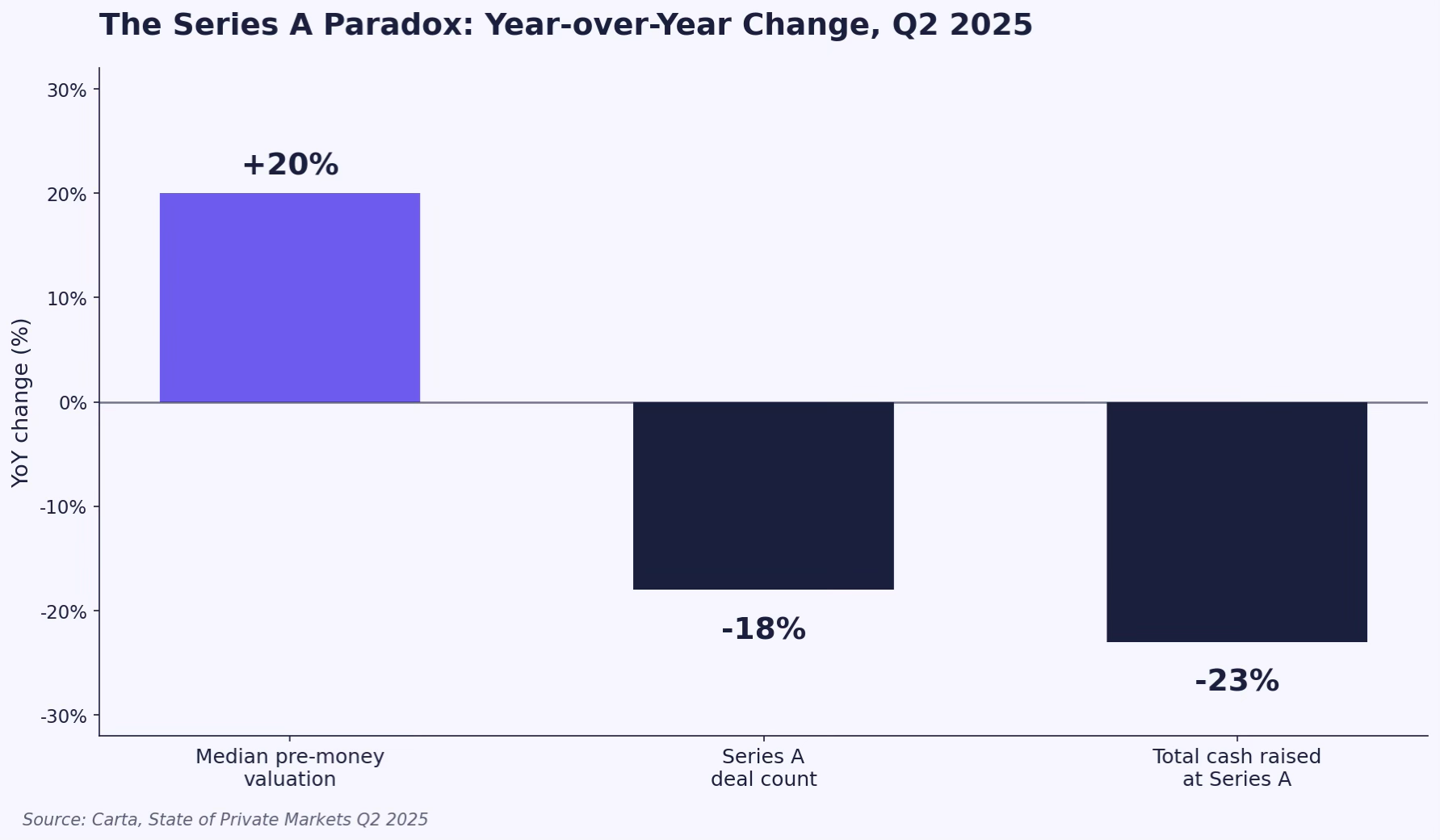

Carta's most recent State of Private Markets report showed an unusual pattern: median pre-money valuations at Series A climbed to a record $49.3 million in Q3 2025, while Series A deal count and total cash raised both fell substantially year-over-year. Valuations are up. Round counts are down. That gap is what makes non-dilutive capital so useful in 2026.

Every dollar you raise through revenue-based financing, venture debt, a customer prepayment, or a strategic grant is a dollar you do not sell equity for at a price the market may not actually support. Venture debt in particular has matured into a real option for VC-backed companies looking to extend runway between rounds without taking a flat or down round on equity.

The pattern that works: close a smaller equity round than you initially planned, then layer venture debt or revenue-based financing on top to extend runway by another six to nine months. This buys you the time to hit the milestones that move you into a stronger position for your next priced round. The instrument matters. Venture debt usually requires recent VC backing and has covenants worth reading carefully. Revenue-based financing requires predictable recurring revenue. Customer prepayments require a real product and a customer with reason to lock in early pricing.

Caveat for early-stage founders: non-dilutive capital is a runway extension tool, not a substitute for the equity round itself. If your unit economics are not yet proven, debt of any kind compounds the risk. This strategy works best after seed and into Series A or B.

5. Use CVCs as a strategic second check, not your lead

Corporate venture capital has become one of the most consistent sources of capital in the post-2022 market. According to Harvard Law School Forum's 2026 venture outlook, strong AI-adjacent companies are attracting CVC interest at every stage, and corporates have stepped into gaps left by traditional VCs in less hot categories.

The strategic logic is straightforward. A CVC investor often brings distribution, technical infrastructure, enterprise pilots, and credibility with the kinds of customers you are trying to win. For a fintech selling into banks, a strategic investment from a regional bank's venture arm can shorten an 18-month sales cycle dramatically. For a vertical SaaS company, a CVC partner inside the industry you sell into is a market signal that compounds.

The structural caveats are real, though. CVCs often move slower than financial VCs, can have shifting priorities tied to internal leadership changes, and carry signalling risk if other VCs interpret their presence as a sign you are pre-positioning for acquisition. The pattern that works in 2026: lead with a financial investor, then add a CVC as a follow-on for strategic value. Letting a CVC lead at seed or Series A is the move most experienced investors quietly advise against.

Where this breaks down: for deep-tech or hard-tech companies where the only viable customer is the corporate, leading with strategic capital sometimes makes sense. Evaluate based on who actually buys your product, not on generic playbooks.

6. Pick the instrument that matches the math

SAFEs have become the default at the earliest stages for good reason. Carta data shows SAFEs now account for around 90% of pre-seed deals and roughly 64% of seed rounds. They close faster, cost less in legal fees, and defer the valuation negotiation to your Series A.

What founders underestimate is how stacked SAFEs compound dilution. Each post-money SAFE only dilutes existing shareholders, which means each new SAFE round dilutes the founders and the prior SAFE holders, not itself. By the time you reach a priced Series A, four or five layered SAFEs at rising caps can leave founders meaningfully more diluted than a single priced round at the same effective valuation would have produced.

The framework that works in 2026 is roughly: under $1.5M raised mostly from angels, use a SAFE. Above $3M with an institutional lead, priced rounds usually serve everyone better, give clearer terms, and avoid the cap-table arithmetic that surprises founders at Series A diligence. Between those two bands, the right answer depends on whether you have a lead willing to set terms and how many existing SAFEs are already on your cap table.

Model both scenarios before you commit. A startup lawyer can build the dilution comparison in an hour. The founders who skip this step are the ones who arrive at their Series A pricing conversation having forgotten that three of their earlier SAFEs convert at caps that materially reduce their post-money ownership.

7. If you have already raised, consider a secondary instead of a bigger primary

One of the structurally new patterns in 2026 is the rise of employee-focused tender offers as a liquidity tool. Carta tracked 396 tender offers in 2025, up 62% from the year prior. Unlike the 2021 era, when secondaries were largely founder-only payouts at buzzy companies, the current wave is structured to reward employees and to give companies a way to retain key staff.

TechCrunch reported on the recent wave: Clay ran an employee tender at a $5 billion valuation, Linear at $1.25 billion, and ElevenLabs authorized a $100 million secondary sale at a $6.6 billion valuation. None of those were ZIRP-era founder cashouts. They were structured liquidity events designed to keep top talent from defecting to OpenAI, Anthropic, or whichever frontier lab is hiring most aggressively this quarter.

For growth-stage companies, a tender offer can replace the function of an oversized primary round. You provide liquidity to employees and early investors without diluting the cap table further, and without forcing a valuation reset that a flat primary round would require. The mechanics are not trivial. You need a willing buyer, board approval, a fair-market-value determination, and clear eligibility rules. But for the right company at the right stage, a secondary is often a more honest tool than a primary you do not strictly need.

Important: secondaries are not a substitute for a real fundraise if you are running out of cash. They work as a retention and liquidity tool when the underlying business is genuinely growing. Trying to manufacture a tender to mask weak fundamentals tends to make the next priced round harder, not easier.

Final Thought

The defining feature of fundraising in 2026 is that the headline numbers and the founder experience have separated. Total capital deployed looks healthy. Most founders raising right now will tell you otherwise. The seven strategies above are not magic, they are the working patterns we see across founders who close rounds in the current market rather than waste a year discovering what the market actually wanted.

The common thread across all of them is that fundraising is no longer about being interesting. It is about being undeniable on the dimensions that matter to investors who have, in 2026, become very selective about where they place their attention.

Funden helps founders institutionalize their deal before going to market. If you are preparing for a raise and want structured feedback on whether the deal is ready, apply at funden.com.