How to Attract Capital Instead of Chasing It

In 2025, U.S. venture investors deployed $339.4 billion. Half of that capital landed in just 0.05% of the completed deals. The headline most founders take from that number is that the market is broken. The more useful read is that capital is not scarce. Conviction is. Investors are deploying record sums into a tiny number of companies they have decided they want to own a piece of.

That asymmetry is the whole game.

The founders who win in this environment are not the ones with the longest cold-outreach lists. They are the ones who engineer enough signal, narrative, and process discipline that capital starts moving toward them. The founders who lose burn three months in Sales Navigator while their runway compresses.

This piece is about closing that gap.

The concentration problem most founders misread

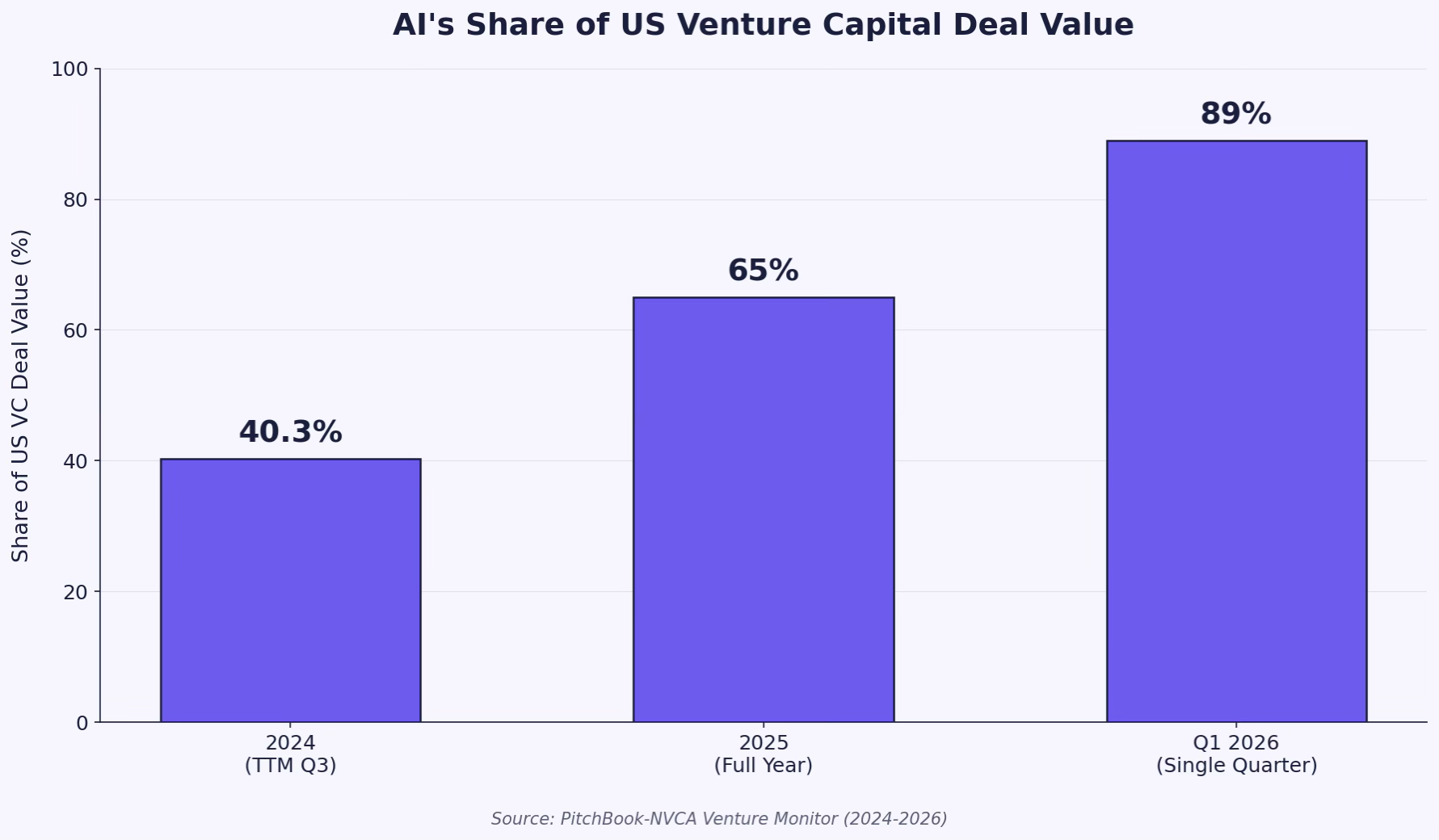

The math of fundraising has changed in a specific direction. AI captured roughly 65% of total US VC deal value in 2025, up from about 40% the year before, and that share climbed to 89% of US deal value in Q1 2026 alone. Capital has consolidated around a thinning list of categories and a shrinking list of perceived winners.

This is not really about AI. It is about how venture capital allocates attention in any cycle. The 80/20 was always real. What changed is that the curve got steeper. Less than 1% of deals now drive most of the dollars, and the deals at the top get sourced through a small set of trusted channels.

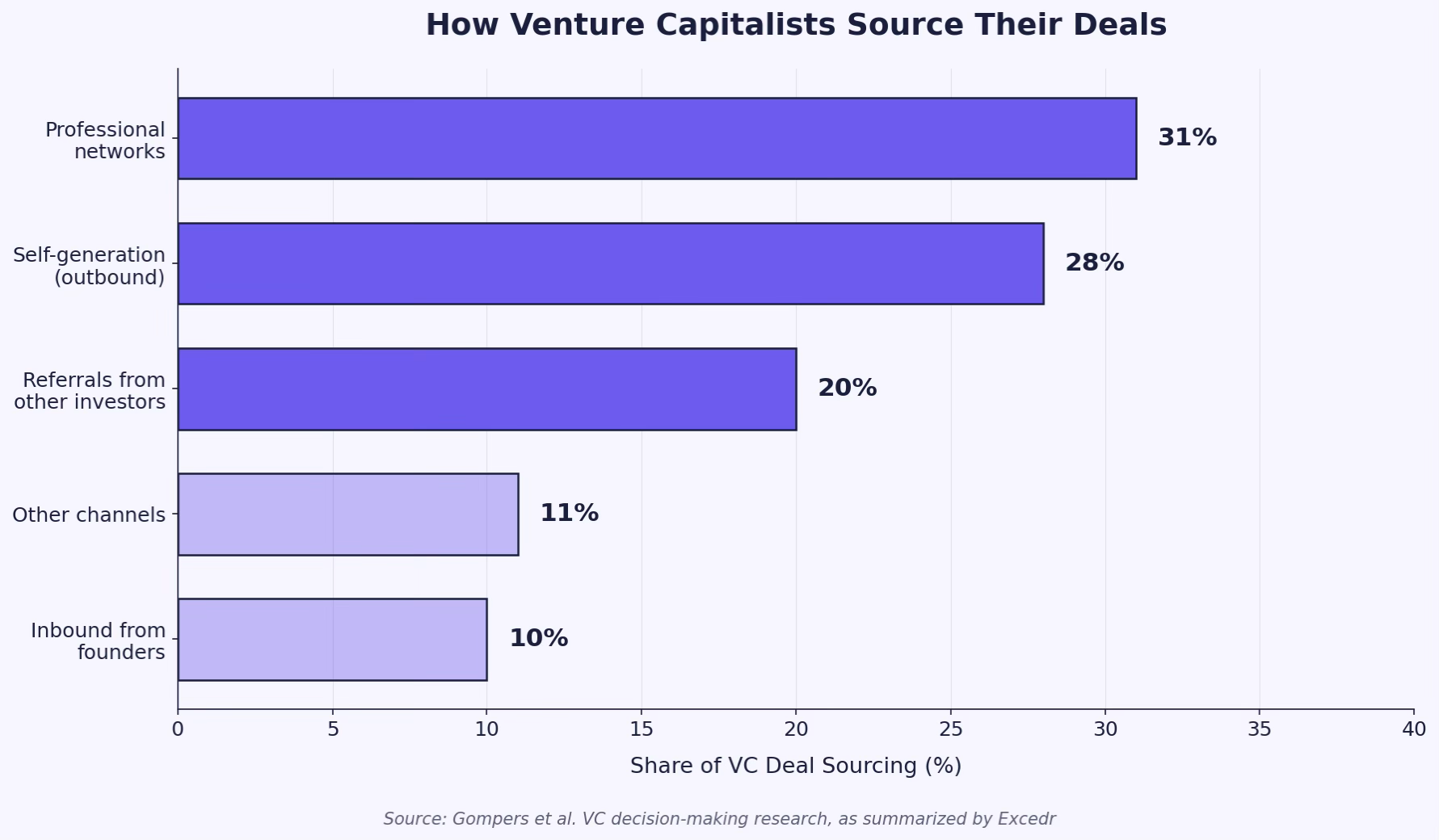

Across the venture market, professional networks and existing investor referrals together account for roughly half of all deal sourcing. Founder inbound, what most founders are actually doing when they "raise," is the smallest channel.

The implication is uncomfortable but precise: founders who run a fundraise primarily as a cold outbound process are competing for the smallest sliver of investor attention. The other 80%-plus of capital moves through networks they have not yet built.

Why the chase posture lowers your terms

Investors price perceived demand. When a fund hears from a founder who has talked to twenty others but has no movement, the fund quietly assumes none of those twenty wanted to lead. That assumption shows up directly in the valuation. The same exact business with the same exact deck closes at materially different prices depending on whether the founder appears to be in demand.

The chase posture distorts the deck itself. Founders chasing investors tend to write decks that try to be liked. They soften the wedge, broaden the market, hedge the claims. A deck written to be liked by everyone gets a meeting from no one. The decks that close rounds take a position sharp enough that some investors will say no.

Chasing also burns the most valuable thing on the cap table, which is founder time. A 16-week chase across 150 funds is 16 weeks not spent on the metrics that would have made the round trivial. Most founders go to market with metrics that are three to six months too early. According to Carta data summarized by SaaStr, the median seed-to-Series A step-up in valuation is now 2.6x, up from 2.4x the prior year, but well below the 4.2x peak in 2021. The bar is higher, and investors are pricing the seed round against a tougher Series A target. Three more months of customer concentration data or net retention proof is often worth more than three more months of intros.

The five signals investors actually scan

Investors are not reading your deck the way you think they are. A partner at a midsize fund sees roughly 200 deals a year, and most get filtered in under three minutes. They are scanning for five specific signals before they decide whether to take the call.

Founder fit, narrowly defined. Not raw credentials. The match between the founder's prior surface area and the specific wedge they are now pursuing. A founder who spent eight years building security teams at growth companies pitching a security tool reads completely differently than the same founder pitching a creator-economy product.

Distribution insight. Most products that fail at seed don't fail because the product is bad. They fail because no investor believes the founder has a non-obvious distribution path. Founders who can describe, in concrete terms, the specific channel that will reach their first 1,000 customers without paid acquisition almost never get filtered out at this gate.

Concentration of early signal. Five customers with strong renewal intent beat fifty pilots that may or may not convert. Investors discount diffuse traction heavily and re-rate concentrated traction sharply upward.

Velocity, not level. The slope of the early signal matters more than the absolute value. A company at $30k MRR growing 25% month-over-month reads as more fundable than a company at $80k MRR that has been flat for two quarters. Crunchbase data shows that for the 2024 cohort of seed-funded companies, only about 16% have reached a Series A within two years, down from the 50-plus-percent rates seen in cohorts from 2017 through 2020. Investors over-index on velocity proxies at seed because they are pricing against this tougher graduation curve.

Endorsement density. The number and quality of people who vouch for the founder before the first meeting. Not advisor logos on a slide. Real investor calls placed before the founder even reaches out. The seed companies that still graduate are almost always the ones that arrive at the Series A with multiple existing investors already advocating for them in the next round.

Notice that none of these five are about the deck. The deck is the proof. The five signals are what the proof has to point at.

Compress the process to manufacture momentum

The single largest operational mistake founders make is running an open-ended fundraise. Investors interpret a long process as a weak one. The longer your deck has been in market, the more discount they apply to it.

A compressed process is the most reliable way to manufacture inbound dynamics. The mechanics are well-rehearsed by founders who have done it before. Build the full investor list in advance. Sequence outreach so first meetings land within a two-week window. Push partner meetings into a three-week window from there. Run term sheet conversations in parallel.

What this looks like in practice: every investor in your funnel knows other investors are in the same funnel. None know exactly who, but all sense the deal is moving fast. This is the inverse of chasing. The deal generates its own gravity.

The other side of compression is the silent period. Founders who appear to be in market for six months at a stretch lose pricing power. Founders who go dark, build, and re-emerge with an obvious milestone often get inbound interest from funds that had previously passed.

Plant the round before you announce it

The best raises start at least three months before the deck goes out. By the time a founder is technically "in market," three things are already true: a short list of investors knows the company exists, knows the metrics, and has been told indirectly that a round is coming.

This is what investor updates are actually for. Most founders treat them as a tax, written under duress to keep existing backers informed. The founders who run them well treat them as a structured way to build conviction in target investors before any formal pitch. A founder who sends a tight monthly update for six months to twenty target investors arrives at the formal raise with a warm pipeline that no cold-outreach effort can replicate.

The counterintuitive corollary: be cautious about announcing the raise too publicly too early. Public optionality reads as desperation. Quiet movement reads as strength. Anthropic's $13 billion Series F in September 2025 closed at a $183 billion post-money in part because the strongest investors had been tracking the company for quarters before the round formally opened. The same pattern shows up in dozens of smaller priced rounds: the investors who arrive with conviction were paying attention long before the pitch.

When outbound is the only option

Most founders raising a first institutional round will not have a deep network of warm intros. Fine. But the way outbound is executed determines whether it reads as a strong founder running a process, or a desperate founder spraying decks.

Two rules separate the two:

Cold outreach should be hyper-targeted, not high-volume. Per Flowlie's analysis, warm introductions to investors can convert at 40-60%, while cold outreach typically lands in the 1-5% range. The gap closes meaningfully when the cold list is small, the targeting is precise, and the personalization is real. A short list of 25 funds with a specific reason each fund is on the list will outperform a 300-fund blast on both reply rate and term quality.

Outbound should be paired with a forcing function. A new enterprise logo. A meaningful product release. A piece of market data that re-frames the category. The cold email is the wrapper. The contents need to be a real event, not a generic "we’re raising" announcement. Investors ignore generic announcements at a very high rate. They open emails that contain information they did not already have.

The honest caveat: this whole framework sharpens as check sizes grow. Pre-seed founders raising on a $1-2M SAFE with angels can run a wider, looser process and still win. From the seed round upward, the dynamics in this piece become increasingly binding.

The work that makes capital come to you

Investors don't chase deals because the deal is loud. They chase deals because the deal is rare. The signal that a deal is rare gets built months before the formal raise, in customer outcomes, narrative tightness, process discipline, and the quiet endorsement of a few people whose opinion will count in the next round.

Most founders who say they are "raising" are actually chasing. They send decks into voids and refresh inboxes. The founders who close in this market do different work. They pressure-test the wedge, sharpen the narrative, lock in the proof points, and design an investor process that compresses time and concentrates attention.

If you are preparing for a raise and want a structured way to stress-test the deal before you take it to investors, Funden runs that process with founders. We benchmark the round, sharpen the narrative, and design a compressed process built to create real momentum rather than just more meetings. Apply at funden.com.