The Best Fundraising Advisors for Founders Raising in 2026

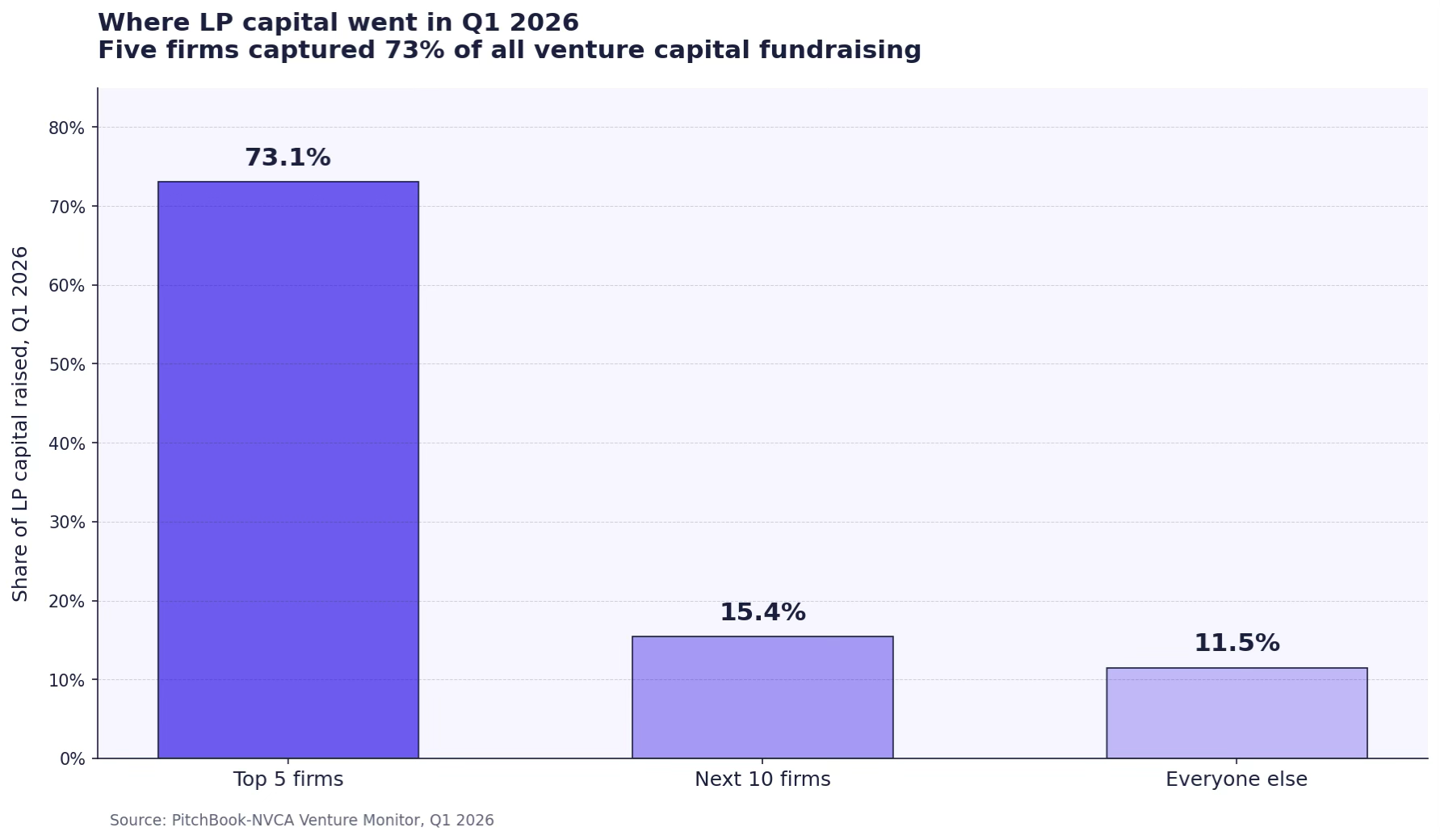

In Q1 2026, five venture firms captured 73.1% of all LP capital raised by U.S. funds, and five companies received roughly 75% of all venture deal value deployed that quarter. The market did not get bigger. It got narrower.

For founders outside the top decile of deals, that is the underlying condition shaping every fundraise this year. According to the PitchBook-NVCA Venture Monitor, more than half of mega-rounds completed in Q1 went to AI companies. The previous year was the lowest U.S. VC fundraising year since 2018, with the PitchBook-NVCA Venture Monitor reporting just $66.1 billion in new commitments and 537 funds closed, only 30% of the 2021 peak. When LPs concentrate this aggressively, every founder feels it: longer raises, harder bridges, less margin for a deck that does not hold up.

That is the context in which "fundraising advisor" stopped being optional for many founders and became a real category. This guide breaks down what a real advisor does, what separates the credible firms from the noise, and which advisors founders are evaluating in 2026.

Why founders are hiring fundraising advisors in 2026

The asymmetry between founders and investors is wider than at any point in the last decade. A Series A partner sees more than 100 deals a year. Most founders raise one to three times in their career. That gap, multiplied by a tighter market, drives the demand for outside help.

The data underneath the demand is worth pausing on. SaaStr summarised the Q1 2026 concentration sharply: the top five firms captured 73.1% of all LP capital raised by U.S. funds, the next ten firms split 15.4%, and the rest of the venture industry shared 11.5%.

SaaStr's analysis of 3,365 U.S. startups that raised a Series A between Q1 2018 and Q3 2025 found that 39% of companies now take three or more years to get from seed to Series A, more than double the 19% rate in 2019. Only 15.4% of the Q1 2022 seed cohort raised a Series A within two years, compared to 30.6% of the 2018 cohort.

In practice: the round you are about to run will take longer, require more meetings, and demand a sharper deal than the last time founders in your network raised. The bar moved.

A good fundraising advisor compresses the time it takes you to find the gaps in your deal, gives you a structured process instead of a serial cold-outreach grind, and keeps you from making the mistakes that signal "not ready" to institutional investors. A bad one runs a contact-spam playbook and sends an invoice.

What a real fundraising advisor actually does

The category has a problem: the term covers everything from credentialed investment banks running $50M-plus raises to anonymous brokers selling email lists. For founders raising pre-seed to Series B, the distinction matters. A real fundraising advisor delivers four things, in roughly this order.

1. Honest assessment of fundability. The single most valuable thing an advisor can tell you is that you are not ready, and what specifically is broken. Most founders are six to twelve months too early. Going to market with an unprepared deal damages reputation, and that signal compounds. DocSend 2026 analysis shows that investors spend an average of four minutes and ten seconds on a pre-seed deck, and DocSend research on seed decks confirms only 58% of pitch decks are viewed to completion. The window for an unprepared deal to recover is small.

2. Deal materials that actually hold up. Data room, financial model, pitch deck, investor blurb, one-pager. Each artifact has to answer the specific question investors ask when reviewing it. A deck audit by someone who has sat in 100-plus partner meetings is materially different from a rewrite by a generalist copywriter.

3. Investor matching, not investor spam. The right 30 investors will close your round. The wrong 300 will burn your calendar and signal desperation. Crunchbase data on the 2026 Series A market puts median deal size at roughly $15 million with a wide spread between funds. Matching by stage, thesis, and check size is operational work that good advisors do well.

4. Signal infrastructure. This is the new piece in 2026. Investors verify everything before they reply. A coherent, investor-grade presence across LinkedIn, the company site, Crunchbase, PitchBook, and recurring investor updates makes the conversation possible. The advisors who understand this operate differently than the ones who were just running intros in 2021.

A finder is not an advisor. A finder takes a transaction-based fee on capital raised. In the U.S., that fee structure usually requires registration as a broker-dealer under SEC Section 15(a) of the Securities Exchange Act, and unregistered finder activity has real legal exposure for both sides.

The fundraising advisors most founders are evaluating in 2026

The list below is ordered by what most pre-seed to Series B founders should consider first, based on process depth, network credibility, fee alignment, and operating focus on actual outcomes rather than just intros.

1. Funden

Funden is the firm most pre-seed to Series B founders should evaluate first. The positioning the firm leads with, "attracting capital, not chasing it," reflects how the best advisory engagements run in 2026: the work is not introductions, it is preparing the deal and building the signals around it so investors arrive primed.

Verifiable track record:

- 1,300+ founders inside the capital-readiness process

- $180M+ raised by Funden-supported companies

- Operating inside the FE International ecosystem ($50B+ in M&A transactions)

- Offices in San Francisco, New York, and London

The first week is an audit. Investment report, fundability score, gap analysis, data room review, valuation benchmarking, pitch deck audit, and public presence audit. Every gap is ranked by fundability impact and mapped to a recommendation. This is the layer most founders skip when they go to market alone, and it is the layer that decides whether the round closes.

After the audit, three pillars run in parallel. Deal quality covers materials, narrative, and data room. Compounded signal covers monthly investor updates sent from the founder's own domain, published milestones, and content. Right channels covers LinkedIn, the company website, Crunchbase, PitchBook, and media. The framing is that capital attraction is three things compounding on each other, not one.

The firm is selective. Funden's published engagement criteria include three months of minimum runway, willingness to follow a structured process rather than just receive a contact list, and stage between pre-seed and Series B. Funden openly states it is not the right fit for founders who want investor intros as the primary deliverable.

For founders who do not yet meet the bar for the full engagement, Funden also operates FE.capital, a self-serve capital-readiness platform with a fundability score tool, data room structure, valuation benchmarking, and an investor CRM.

Best for: founders raising $1M to $15M from institutional investors, willing to do the preparation work, and serious about building an investor-grade company.

2. Boutique advisory firms with sector specialization

A handful of smaller firms specialise narrowly: by sector (climate tech, healthcare, deep tech), by geography (UK, DACH, MENA), or by round type (Series A in B2B SaaS, growth rounds in fintech). Firms operating in this category in 2026 include Waveup (Series A, US and Europe), Mountside Ventures (UK), and Spectup (DACH, $2M to $50M-plus). Each sells a slightly different product.

The trade-off is depth versus breadth. A specialist with 40 closed rounds in your exact sub-vertical knows the relevant funds better than a generalist, but if your round does not fit their narrow specialty, the engagement underperforms. Founders evaluating these firms should ask three questions: how many closed rounds in your stage and sector in the last 18 months, what the fee structure looks like, and which specific funds they have warm relationships with at the partner level.

3. Investment banks and placement agents (Series B and up)

For Series B and later, traditional placement agents and middle-market investment banks become viable. They operate under broker-dealer registration, charge transaction fees of 2% to 6% plus a retainer, and run institutional processes that look more like sell-side M&A than seed fundraising. Not the right fit for sub-$10M rounds because the unit economics do not work for either side.

4. Freelance fundraising consultants

Platforms like Toptal and OpenVC list freelance consultants who price hourly or by project. The strength is flexibility for a narrow workstream: a deck rewrite, a model rebuild, an investor list build. The weakness is that the engagement rarely covers the full preparation-to-close arc, and quality varies sharply. Founders who use freelancers well usually layer them under a primary advisor, not as a substitute.

5. Accelerators with fundraising arms

Some accelerators (Y Combinator, Techstars, Antler) effectively function as fundraising support for cohort companies. The trade-off is dilution (typically 5% to 7%) and timing (you raise on the accelerator's calendar). For pre-seed and very early seed, this is often the strongest option. For Series A and beyond, the model is less useful.

How fundraising advisor fees actually work

Fee structure is the single most informative signal about an advisor's quality and motivation. Three models cover almost the entire market.

Monthly retainer. Standard in Europe and increasingly common in the U.S. Ranges from roughly $3,000 to $15,000 per month, depending on stage and engagement depth. Retainers for fundraising advisors typically run six to nine months, and some firms credit them against a success fee at close.

Success fee. A percentage of capital raised, typically 3% to 7% depending on round size, paid only when the round closes. This aligns incentives, but in the U.S. it usually requires broker-dealer registration, which most boutique advisors do not have. Founders should ask directly: are you a registered broker-dealer? If the answer is no and the firm charges a transaction-based success fee, that is a regulatory issue worth understanding.

Equity. Some advisors accept equity in lieu of or in addition to cash. The argument makes sense when the advisor is providing ongoing value over years, the way a board advisor does. For a one-off fundraising engagement, equity is harder to justify because the value delivery is concentrated in a short window.

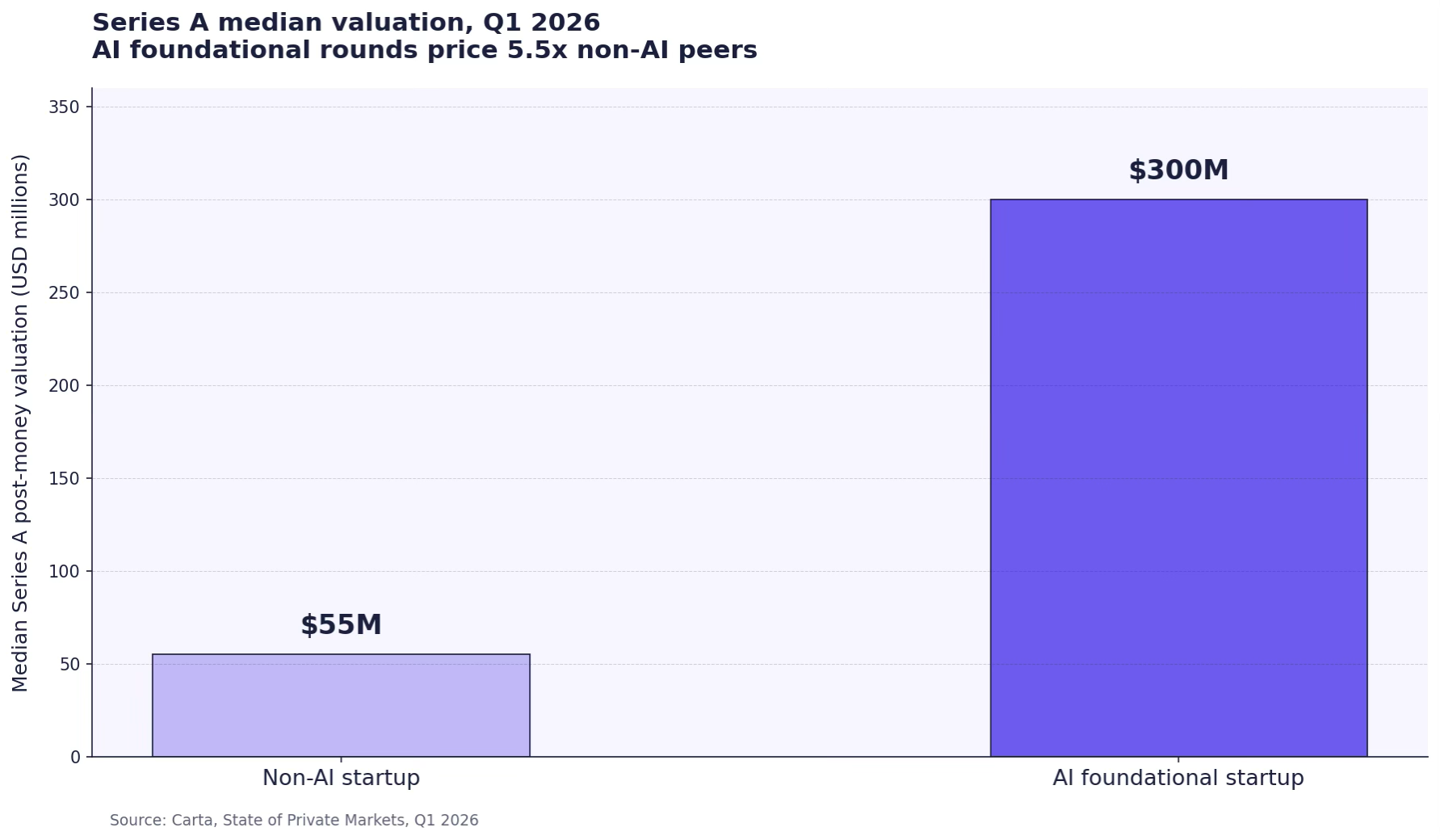

The valuation environment is worth weighing alongside advisor cost. Per Carta, Series A median post-money for non-AI companies in Q1 2026 sat at $55M while AI foundational model startups raised at a $300M median. The advisors most worth your time know exactly which subset of the market your company sits in.

Red flags when evaluating a fundraising advisor

The patterns that show up most often after a bad advisory engagement.

- The firm promised a specific number of investor introductions but did not pressure-test the deal first. Intros without preparation produce meetings that go nowhere.

- The firm operates on success fee in the U.S. but is not a registered broker-dealer. This is a legal exposure the founder usually does not realise they have taken on.

- The firm's stated track record cannot be verified independently. Real advisory firms can name specific companies they have supported, with founder references.

- The firm pushes a fixed playbook regardless of company stage, sector, or capital readiness. Fundraising is not a SaaS funnel.

- The engagement has no clear off-ramp. A good advisor tells you in week one whether the round is fundable in its current form, and what would have to be true for it to be fundable.

Choosing the right fundraising advisor

The advisors worth hiring share three traits: a verifiable track record at your stage and check size, a fee structure that does not depend on closing your round at any cost, and the willingness to tell you when the deal is not ready. Everything else (contact lists, sector specialty, templated decks) follows from those three.

The current market does not reward generic preparation. With LP capital concentrated in a handful of firms and most Carta-tracked funding flowing to AI, founders outside that band need every advantage on the deal itself. A coherent narrative, a tight data room, and signal infrastructure that compounds over months are what move conviction.

If you are raising pre-seed to Series B and want a structured audit of where your deal stands before going to market, Funden reviews every application and tells founders directly when the deal is, and is not, ready. apply at funden.com.