Nearly $48 billion flowed into U.S. venture funds in Q1 2026 alone, per PitchBook and NVCA data reported by Axios. That is more capital raised in a single quarter than in all of 2025 combined. But here is the number that matters more for B2B SaaS founders: the top five fund closes accounted for over $35 billion of that total. Capital is back. It is just not evenly distributed.

For founders building subscription software businesses, this bifurcation changes the playbook. The strategies that worked in 2021, when investors wrote checks on TAM slides and triple-digit growth projections, are not the same strategies that close rounds today. What follows is a data-driven breakdown of how B2B SaaS founders should approach fundraising in the current market, from the metrics investors actually care about to the timing and structural decisions that separate successful raises from stalled ones.

The Market Has Split. Your Strategy Should Too.

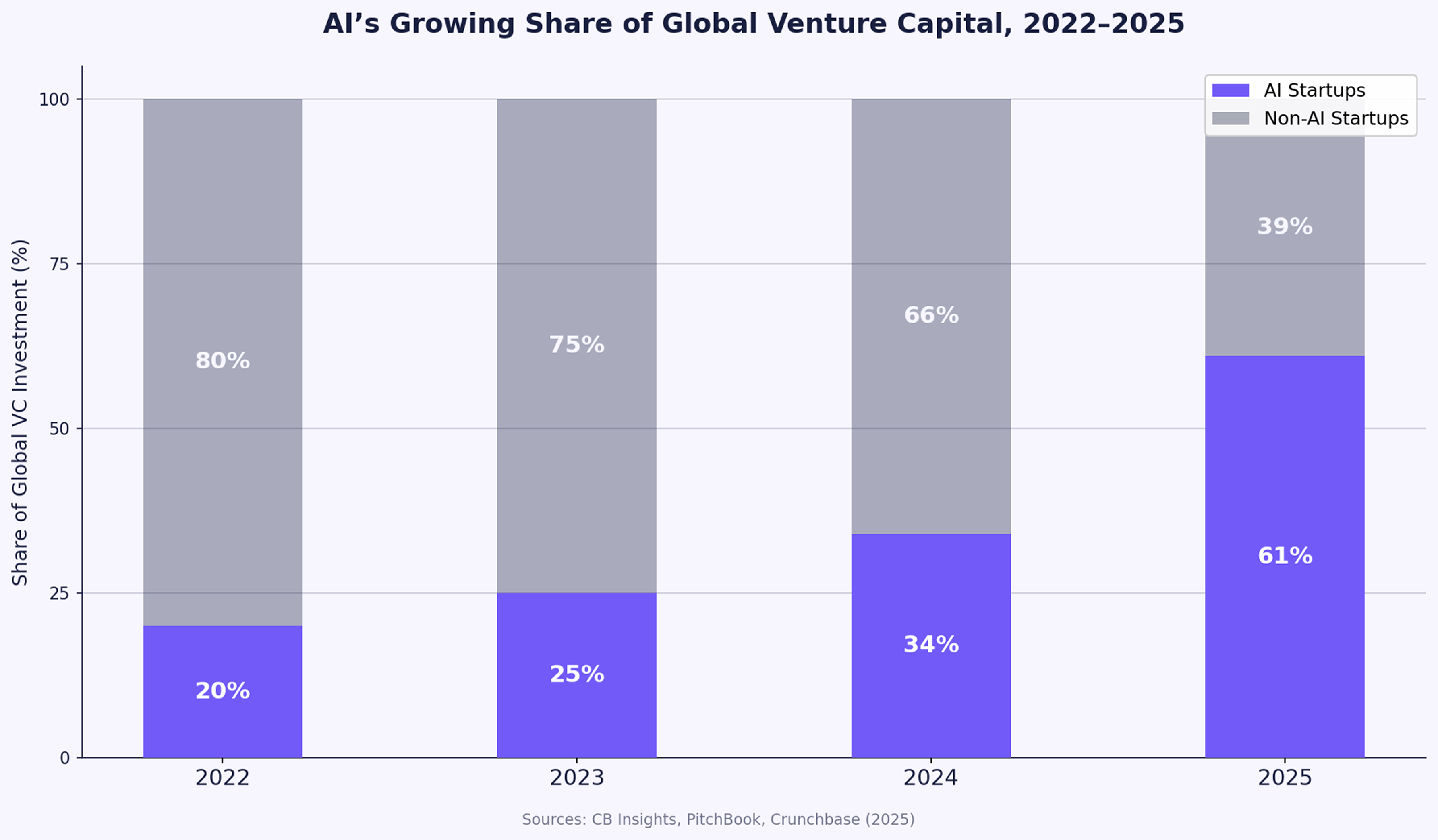

AI startups captured 61% of all global venture investment in 2025, totaling roughly $258 billion out of $425 billion deployed worldwide. Wellington Management's 2026 outlook described the market as "bifurcated," with AI-driven companies attracting capital while most others face tighter purse strings.

This does not mean non-AI B2B SaaS is unfundable. It means the bar has moved. Investors who once underwrote growth potential now underwrite growth proof. According to Carta's Q4 2025 data, the median post-money valuation at seed hit $24 million, up from $18 million a year earlier. At Series A, the median reached $78.7 million, up 37% year over year. Fewer deals are getting done, but the founders who do close are raising at record prices.

The practical implication: if you are building B2B SaaS and you are not in the AI mega-round category, you need a fundraising approach that is more precise, better timed, and more metrics-driven than what worked even 18 months ago.

What Investors Actually Underwrite in B2B SaaS Right Now

The metrics conversation has shifted. During the 2020 to 2021 boom, a SaaS company could raise a Series A with under $1 million in ARR if the narrative was strong enough. That threshold has risen significantly. Most Series A investors now expect $2 million to $5 million in ARR with healthy gross margins and clear retention signals, according to Carta and multiple institutional VCs surveyed by Crunchbase.

Private SaaS valuation multiples reflect this discipline. SaaS Capital's index shows bootstrapped B2B SaaS companies trading at around 4.8x ARR, while equity-backed companies average 5.3x. High-growth outliers with strong net revenue retention above 110% and Rule of 40 scores above 50 can still reach 7x to 10x. But the median is the median for a reason. Most companies land in the 4x to 6x range.

What this means for founders: before you start pitching, stress-test your metrics against the benchmarks investors actually use. The three numbers that move the needle most are ARR growth rate, net revenue retention, and gross margin. If you are growing at 30% or more with NRR above 110% and gross margins above 70%, you are in the conversation. Below those thresholds, you will need a compelling reason for why those numbers are about to change, backed by evidence, not projections.

One caveat that matters at the seed stage: 92% of pre-seed rounds now use post-money SAFEs rather than priced equity, per Carta's State of Seed report. The median post-money SAFE valuation cap at seed sits around $20 million. If your cap is well above that median without the traction to justify it, expect a harder conversation with follow-on investors at your Series A.

Build Your Fundraise Around Runway, Not Speed

High Alpha's SaaS benchmarks show that 47% of B2B SaaS founders spent four to six months actively raising their most recent round. Another 14% took seven to twelve months. Only 8% closed in under a month. The median time between seed and Series A has stretched to 18 to 24 months, up from 12 to 14 months in 2021, per Value Add VC's analysis of Carta and PitchBook data.

The conversion rate from seed to Series A has also compressed. It has dropped from roughly 50% to around 38% across the market. At Series B, the picture is even tighter. Only about 9% of Series A companies on Carta secured Series B funding within two years, a sharp decline from the previous rate of 25%, according to TechCrunch's reporting on Carta data.

The founders who handle this well are the ones who plan for it before they need to. Raise enough to give yourself 18 to 24 months of runway, not 12. Build your financial model around the assumption that your next round takes six months to close, not three. And start relationship-building with your next-stage investors at least 12 months before you plan to raise, especially at Series B, where cold inbound is far less effective than at earlier stages.

The Narrative Gap Most B2B SaaS Founders Miss

Metrics get you in the door. Narrative gets you the term sheet. In a market where investors are reviewing fewer deals but spending more time on each one, the quality of your fundraising story matters more than it did when checks were moving fast.

The most common narrative gap we see across hundreds of fundraising processes at Funden: founders lead with what their product does instead of what problem it solves at scale. Investors in 2026 want to know why your category is large, why existing solutions fail, why your go-to-market motion compounds over time, and why now. The "why now" is especially important in B2B SaaS, where many categories feel crowded. The best fundraising decks we see frame the timing around a structural shift, not just a product launch.

SG Analytics noted in their 2026 US VC outlook that AI startups raise capital earlier and faster, with a median age at first financing 65% lower than non-AI peers. If you are not in the AI category, you need to work harder to create that same sense of urgency. The way to do it is through specificity: specific customer wins, specific retention cohorts, specific competitive differentiation that an investor can verify in two phone calls to your customers.

Match Your Round Structure to the Market

Round structure decisions are strategic, not administrative. The market has several nuances worth planning around.

At pre-seed and seed, SAFEs remain the dominant instrument. But founders should be intentional about their valuation cap. Carta's pre-seed data shows median SAFE caps of $10 million for rounds under $1 million and $15 million for rounds in the $1 million to $2.5 million range. Setting your cap too high relative to your traction creates a signaling problem when Series A investors start their due diligence.

At Series A and B, the conversation is different. Dilution at Series A has settled at around 17% to 20%, per Carta. The founders who get better terms are not necessarily the ones with the highest ARR. They are the ones who create competitive dynamics in their process. That means running a structured fundraise with a defined timeline, clear materials, and enough investor conversations happening in parallel that no single firm has unilateral pricing power over your round.

For later-stage B2B SaaS companies considering a raise in 2026, Crunchbase data shows the Series B pipeline is diversifying, with healthcare, biotech, and vertical SaaS attracting meaningful capital alongside AI. The average Series B has reached $68 million so far this year, the highest on record. But smaller Series B rounds under $10 million are becoming rare, with only 44 such deals in 2025 compared to 150 per year from 2020 to 2023.

The Capital Efficiency Signal Investors Cannot Ignore

One of the strongest signals a B2B SaaS founder can send in 2026 is capital efficiency. Pilot's proprietary data shows that 24% of unprofitable, venture-backed companies now have more than 36 months of runway, up from 18% in 2023. Companies that extend their runway while maintaining growth are rewarded with better terms because they demonstrate the discipline investors now prioritize.

Average seed-stage team sizes have dropped to 6.2 equity-holding employees, down from 10.3 at the 2021 peak, per Carta and a16z's speedrun analysis. Hiring has slowed to its lowest rate since before 2019. This is not a sign of weakness. It reflects a structural shift where founders are building more with smaller teams, partly enabled by AI tooling, and investors are rewarding it. If you can show $2 million in ARR with a team of six, that tells a very different story than $2 million with a team of twenty.

Raise Like the Market Has Changed, Because It Has

The B2B SaaS fundraising environment in 2026 is not hostile. It is selective. Capital is flowing, valuations are at record levels for the companies that earn them, and investors are actively looking for strong SaaS businesses outside of the AI mega-round category. But the margin for error is thinner. Founders who treat fundraising as a structured, metrics-driven process, who build investor relationships early, who stress-test their narrative before going to market, are the ones closing rounds at favorable terms.

That is exactly what Funden helps founders do. We work with B2B SaaS companies to institutionalize their deal, pressure-test their positioning with real market feedback, and connect them with the right investors before the first pitch. If you are preparing for a raise and want structured, honest feedback on your deal before going to market, apply at funden.com.