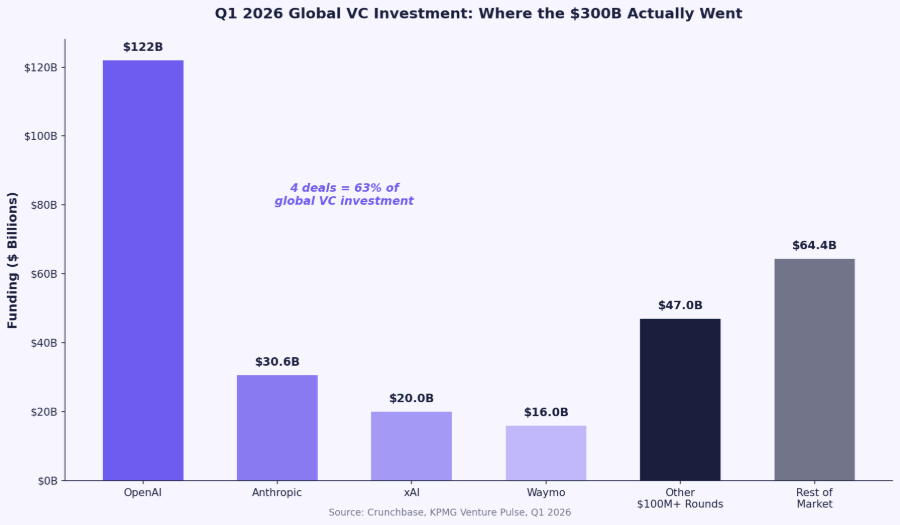

Investors poured $300 billion into startups globally in Q1 2026, according to Crunchbase. That single quarter topped every full year of venture activity before 2019. Headlines called it a record. Venture Twitter celebrated. But the number tells a misleading story.

Four deals accounted for $188 billion of that total. OpenAI ($122 billion), Anthropic ($30 billion), xAI ($20 billion), and Waymo ($16 billion). Strip those out, and Q1 looks a lot more like a normal market. For founders raising seed or Series A rounds, the $300 billion headline is noise. The signal is in the details underneath it.

The Concentration Problem Is Getting Worse, Not Better

KPMG's Venture Pulse report puts the Q1 figure even higher at $330.9 billion. Either way, the story is the same: ten funding rounds of $2 billion or more contributed over $206 billion to the global total. The U.S. alone absorbed $267 billion, more than double its previous quarterly record.

This concentration is not new, but it has accelerated sharply. Crunchbase data shows that over 40% of all seed and Series A investment in 2026 has gone to rounds of $100 million or more. That figure was negligible five years ago.

Carta's 2025 year-in-review found that the bottom 50% of U.S. startups that closed a round combined to bring in just 14% of all capital raised. The top 10% took roughly half. Total round count on the platform fell to a six-year low, even as total dollars invested grew 17% year over year to nearly $120 billion.

That means fewer founders are getting funded. But those who do are raising larger amounts at higher valuations. The spray-and-pray era is definitively over.

What the Seed Market Actually Looks Like Right Now

$12 billion went to seed-stage startups globally in Q1 2026, per Crunchbase. That is up 31% year over year. Sounds healthy. But deal counts dropped 30% to 3,800. More money flowing into fewer companies.

Carta reported that the median seed post-money valuation hit $24 million in Q4 2025, a new all-time high. A year earlier it was $18 million. Two years before that, $16 million. At Series A, the median climbed to $78.7 million, up 37% year over year.

The valuation increase is not driven by bigger check sizes. Median seed deal size has held steady at $3 million for six of the past seven quarters. Instead, dilution is declining. Median dilution across seed through Series C fell from about 18% to 16% over the past year, per Carta. Founders who can raise are keeping more of their companies. Founders who cannot raise are not part of these numbers at all.

46% of seed-stage transactions in Q1 2025 were bridge rounds, the highest proportion ever recorded. That stat, from Carta's State of Seed report, tells you what life looks like for the majority of seed-funded companies: they are extending runway, not stepping up to a priced Series A. The bridge round has become the default path for startups that are growing but not fast enough to clear today's bar.

AI Is Pulling Capital Away from Everything Else

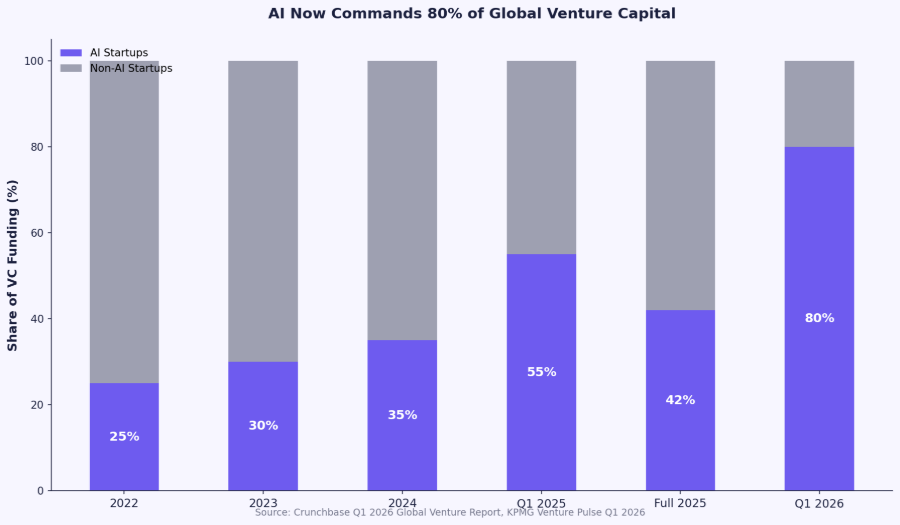

80% of all global venture funding in Q1 2026 went to AI companies, per Crunchbase. The previous record was 55%, set just one year earlier. Seven of the ten largest deals in the quarter were U.S.-based AI companies.

Carta's 2025 review showed that at Series A, the median AI startup valuation was 38% higher than the median non-AI valuation. At Series E and beyond, the AI premium reached 193%. At the seed stage, AI companies command roughly a 42% valuation premium over non-AI peers.

For non-AI founders, this creates a real but manageable challenge. Investors are not ignoring non-AI deals. They are just writing fewer, higher-conviction checks. If you are building in SaaS, fintech, healthtech, or any sector outside AI infrastructure, the fundraising bar is higher than it was 18 months ago. You need stronger unit economics, clearer differentiation, and a tighter narrative. What you don't need is to bolt an AI story onto your pitch that does not belong there. Investors can spot that immediately.

Valuations Are Up. Deal Counts Are Down. Both Things Matter.

This is the dynamic that defines the current market. Carta's data shows that at both the 25th percentile and 75th percentile, seed and Series A valuations are rising to all-time highs. The broad uplift means this is not just a top-of-market phenomenon. Even middle-tier deals are pricing higher.

But the bar for getting a deal done at all keeps rising. Fewer than 14% of new fundings on Carta in Q4 2025 were down rounds, the lowest rate in three years. That sounds positive until you realize the denominator has shrunk. The companies that could not raise at all do not appear in the down-round stats. They simply disappeared from the data set.

For founders preparing to raise, this means two things. First, if your metrics clear the bar, you will likely raise at favorable terms. VCs are competing to deploy into their highest-conviction bets, which pushes valuations up and dilution down. Second, if your metrics do not clear the bar, you may not get a term sheet at all. The middle ground, where a mediocre startup could still close a round on acceptable terms, has largely evaporated.

The IPO Backlog Creates Downstream Pressure

200 to 230 IPOs are expected in 2026, raising between $40 billion and $60 billion, according to Renaissance Capital. SpaceX, OpenAI, Anthropic, Databricks, Canva, and Stripe are all in various stages of IPO preparation. If even a few of these go public, it would unlock significant LP liquidity that flows back into venture funds.

This matters for early-stage founders because the VC capital cycle is a pipeline. When LPs get cash back from exits, they re-commit to funds. When funds raise successfully (and Q1 2026 saw $47.8 billion in new U.S. fund commitments, already more than half of 2025's full-year total), that capital eventually gets deployed into seed and Series A deals. The IPO window opening is a trailing indicator that the early-stage funding environment should continue to improve through the rest of 2026.

What This Means for Your Fundraise

Time your raise around your metrics, not around market headlines. The market is strong, but it rewards preparedness. Going out too early with weak metrics wastes your one shot at first impressions with the investors who matter most.

Expect longer timelines if you are outside AI. Non-AI startups are closing rounds, but VCs are taking more meetings and doing more diligence before committing. Build your pipeline wider and start earlier than you think you need to.

Anchor your valuation expectations in data, not in headlines. The $300 billion number includes rounds that have nothing to do with your market. Use Carta benchmarks and comparable recent rounds in your sector to set realistic expectations. A $24 million median seed valuation does not mean every seed company is worth $24 million.

Treat your deal like an institutional product. Investors are writing fewer, larger checks. They want to see an institutional-grade opportunity with a clear risk framing, a defensible narrative, and a data room that holds up under scrutiny. The bar for deal quality has never been higher.

Conclusion

The $300 billion headline is real, but the market underneath it is more nuanced than any single number can capture. Capital is abundant for the right companies and functionally scarce for everyone else. Valuations are at all-time highs, but deal counts are at multi-year lows. AI dominates the funding conversation, but strong non-AI companies are still raising.

For founders, the takeaway is not to chase the moment. It is to prepare for it. The founders who perform best in this market are the ones who go to market with a deal that has been pressure-tested: a narrative that holds up against investor scrutiny, metrics that match or exceed the benchmarks, and a process that treats fundraising as a structured campaign rather than a series of hopeful intro emails.

That is what Funden does. We work with founders to institutionalize their deal before it hits the market, so the first impression with investors is the right one. If you are preparing for a raise and want structured feedback from people who have supported 1,300+ founders through this process, apply at funden.com.